Explainable AI in Credit Risk: From Regulatory Requirement to Competitive Advantage

Key Takeaways

- Explainable AI is no longer optional. The EU AI Act, FCA Consumer Duty, and PRA SS1/23 all require lenders to show why automated credit decisions were made.

- Explainability does not cost performance. XGBoost with SHAP explanation achieves a Gini coefficient within 2 points of the best black-box models — while meeting every current regulatory standard.

- The commercial benefits go beyond compliance. Explainable models improve feature engineering, accelerate policy iteration, support fair lending, and turn declined customers into recoverable ones.

Explainable AI in credit risk has moved from a nice idea to a legal requirement. Three major regulatory frameworks now demand it. The EU AI Act, FCA Consumer Duty, and PRA SS1/23 all require lenders to show how their models work and why decisions were made.

But something else is happening too. The institutions that have invested most seriously in model explainability have found it improves their models. Cleaner features, faster iteration, better fair lending controls — these benefits emerge naturally from building AI that can be inspected.

This article covers what explainable AI means for lenders in practice, which frameworks apply, and how to build it in a way that strengthens your AI in credit risk management.

Why Explainability Is Now Central to AI in Credit Risk Management

Credit decisions affect people's lives. A small business refused a loan at the wrong moment. A consumer denied a mortgage they could afford. Regulators have always expected lenders to be able to justify decisions. What has changed is the technology.

Traditional scorecards were transparent by design. A points system is easy to explain, audit, and challenge. Modern ML models — gradient boosted trees, neural networks, ensemble methods — can be far more predictive. But their internal logic is harder to see.

That gap between performance and transparency created risk. Regulators noticed. The result is a set of overlapping frameworks that make explainability a hard requirement for any lender using AI in credit decisions.

Regulatory Pressure and What It Means for Artificial Intelligence in Credit

Three frameworks now shape what explainable AI in finance must look like for UK and EU lenders. Each targets a different aspect of the problem.

EU AI Act: The High-Risk Classification

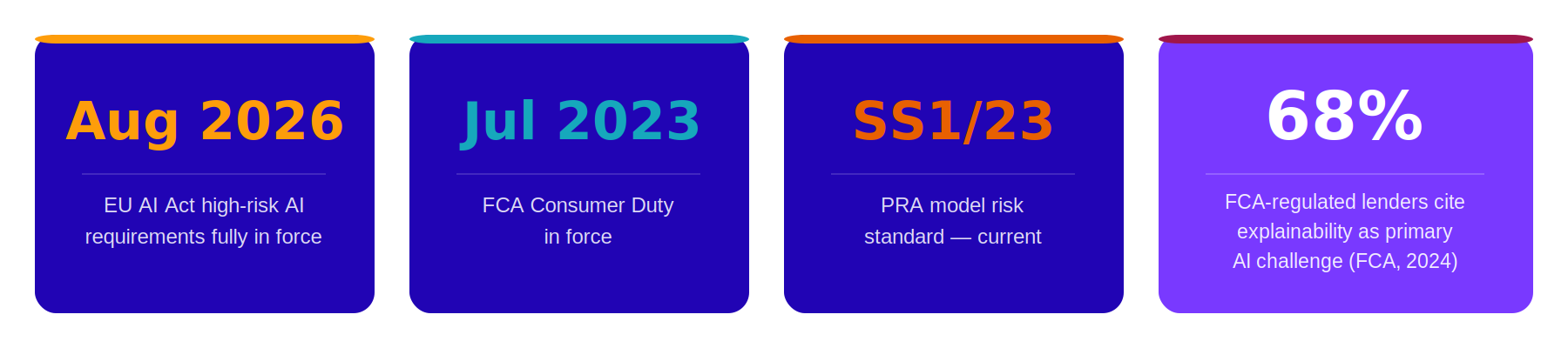

The EU AI Act classifies AI systems used for credit scoring as high-risk under Annex III. That means full transparency requirements, human oversight at decision points, and continuous monitoring. A model whose logic cannot be inspected fails this standard. Full requirements apply from August 2026.

FCA Consumer Duty: Good Outcomes

Consumer Duty requires firms to show their products produce fair outcomes for customers. For AI-driven credit decisions, this means being able to explain why a decision was reached. It also means identifying segments experiencing systematically poor outcomes — which requires the ability to look inside model behaviour across the portfolio.

PRA SS1/23: Model Documentation

SS1/23 sets the current supervisory standard for model risk management. It requires comprehensive documentation: model logic, assumptions, limitations, and intended use. For ML models specifically, it extends to feature importance, stability under distributional shift, and the conditions under which outputs should not be trusted.

For a broader view of how these frameworks apply, see our article on explainable AI in modern lending.

How Predictive Modelling Tools for Credit Risk Analysis Benefit from XAI

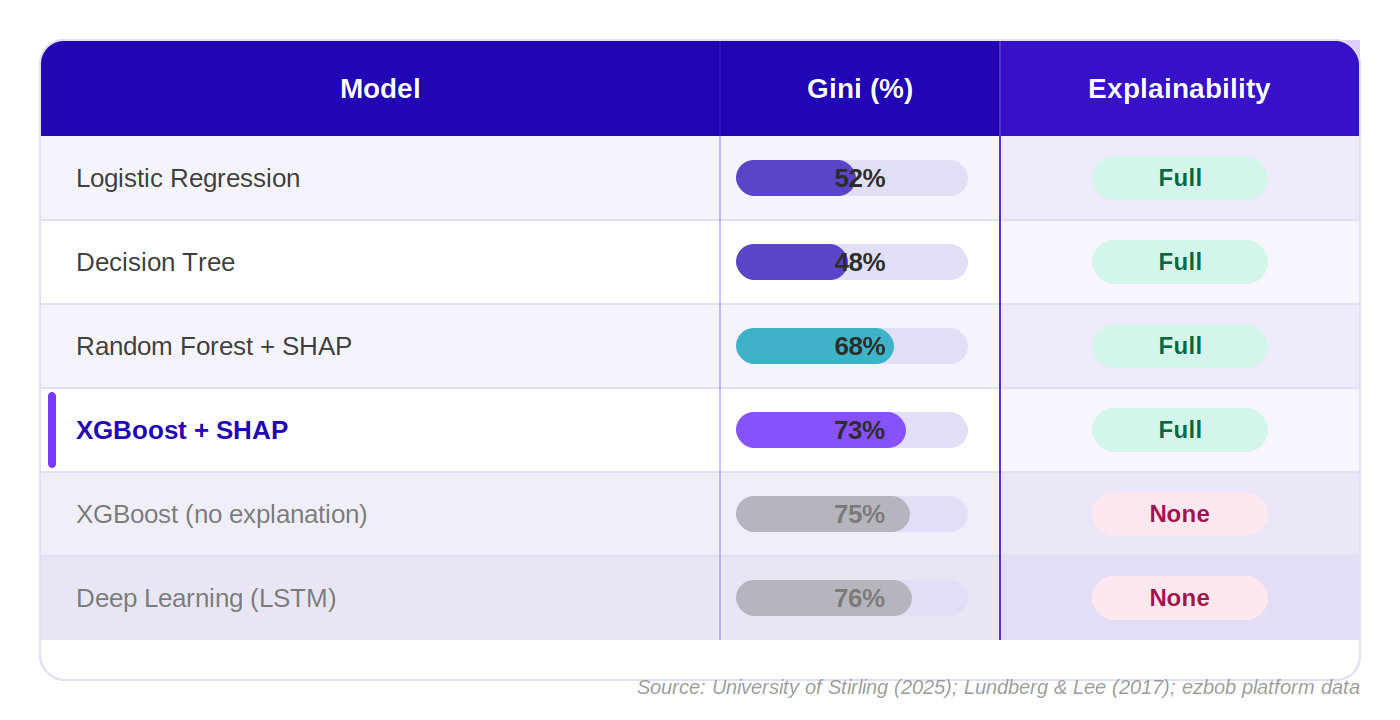

There is a common assumption that explainability costs performance. That explainable models are simpler models, and simpler models predict less well. The data does not support this.

Research Insight: Performance vs. Explainability in SME Credit Models

Recent research examined explainable AI for credit default prediction in government-guaranteed SME lending — a domain where decisions affect not just borrowers, but public money.

The key finding: XGBoost with SHAP explanation achieved a Gini coefficient within 2 percentage points of the best black-box model. For regulated lending, a model that is 2 points less discriminating but fully explainable under SS1/23, Consumer Duty, and the EU AI Act carries materially lower compliance risk. The performance trade-off is small. The compliance benefit is large.

A second finding matters too. Building for explainability improves feature engineering. When you must explain why a feature is in the model, you are forced to understand what it actually measures. This process removes spurious correlations and surfaces better features that a black-box search might have missed.

The two main methods for explainable AI in finance each have specific strengths.

SHAP (SHapley Additive Explanations)

SHAP assigns each feature a value that represents its contribution to a specific prediction. For credit models, SHAP works at two levels. At the individual level, it explains each decision in terms the applicant can understand. At the model level, it shows how the model behaves across all applicants — which regulators and risk managers need for validation.

LIME (Local Interpretable Model-Agnostic Explanations)

LIME builds a simple surrogate model around a single prediction to explain its local behaviour. It is faster than full SHAP computation for large feature sets. The trade-off is less stability — small changes to input data can shift the explanation. For high-stakes individual decisions, SHAP is generally preferred.

Turning AI Credit Insights Into Competitive Advantage

Compliance is the floor, not the ceiling. Lenders that have built explainable AI properly have found it creates commercial value beyond regulatory satisfaction.

Better Customer Journeys

An applicant told exactly why they were declined — and what would need to change for them to be accepted — is a recoverable customer. An applicant told only that the model said no is a lost one. SHAP-based adverse action notices make the difference. They are also a Consumer Duty requirement.

Faster Policy Iteration

When risk managers can see model behaviour at the feature level, policy adjustments are faster and safer. In opaque model regimes, the same changes require full retraining and validation cycles. Explainable AI compresses that timeline.

Fair Lending Controls

SHAP attribution makes it straightforward to test whether protected characteristics — or proxies for them — are driving adverse decisions. This is increasingly expected by the FCA and required under the Equality Act for AI-driven decisions.

Smarter Features

The discipline of explaining model decisions exposes weak features. Spurious correlations that survive a black-box search become obvious when you must explain them to a validator. Over time, this produces leaner, more robust models with better out-of-sample stability.

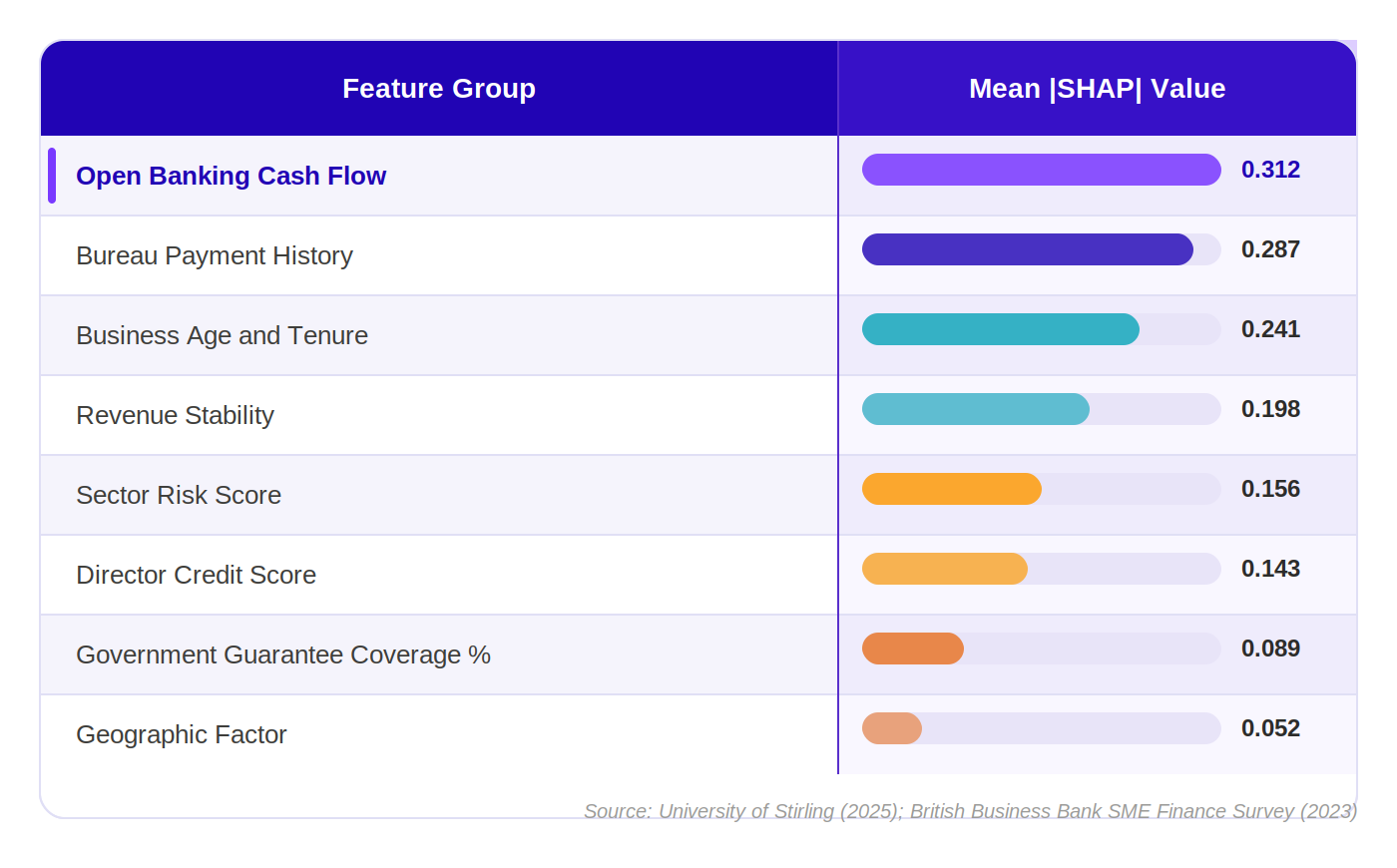

Top Predictors in an SME Credit Default Model

The table below shows mean absolute SHAP values by feature group from an illustrative government-guaranteed SME lending portfolio. Open banking cash flow leads the ranking — reinforcing why open finance data integration is a strategic priority alongside model explainability.

Building Explainability Into Your AI in Banking Risk Management

Explainability is not something you bolt on after a model is built. It needs to be part of the architecture from the start. In practice, this means working across three layers.

Layer 1 — Individual Explanation (Decision Level)

Every automated credit decision should produce a plain-language explanation based on SHAP values. This satisfies GDPR right-to-explanation requirements, Consumer Duty disclosure obligations, and fair lending controls. It also feeds adverse action notices directly.

Layer 2 — Model Attribution (Model Level)

Global feature importance analysis, partial dependence plots, and interaction effects give validators, risk managers, and regulators a view of how the model behaves across the full input distribution. This is the layer that supports SS1/23 independent validation and EU AI Act documentation.

Layer 3 — Behavioural Monitoring (Portfolio Level)

Models drift. Populations change, economic conditions are updated, and data quality issues all degrade model behaviour over time. A monitoring layer that tracks feature importance stability, performance metrics, and outcome disparities across protected characteristic proxies generates early warnings before problems become incidents.

For a practical guide to applying these layers in a lending context, see our article on AI-automated credit decisioning.

Frequently Asked Questions

- What is explainable AI in credit risk?

Explainable AI in credit risk refers to models and methods that can show why a credit decision was made — not just what the outcome was. Rather than producing a score from a process nobody can inspect, explainable AI identifies which factors drove the result, how much each one contributed, and what would need to change for a different outcome. Tools like SHAP and LIME are the most widely used methods.

- Why do regulators require explainability in AI credit decisions?

Three frameworks now require it in practice. FCA Consumer Duty demands that firms demonstrate good outcomes for customers — which means being able to justify decisions. PRA SS1/23 requires full model documentation including feature importance for ML models. The EU AI Act classifies credit-scoring AI as high-risk, requiring transparency and human oversight. Together, these make explainability a compliance requirement, not just good practice.

- How does explainable AI differ from traditional credit scoring?

Traditional scorecards use a fixed set of weighted variables — points for payment history, points for credit utilisation, and so on. The logic is visible by design. Modern ML models can find far more complex patterns across many more variables, but the internal workings are harder to inspect. Explainable AI applies techniques like SHAP to make those complex models as transparent as a traditional scorecard, without forcing a return to simpler methods.

- What are the main risks of using black-box AI models in lending?

Four risks stand out. First, regulatory non-compliance: opaque models cannot satisfy Consumer Duty, SS1/23, or the EU AI Act. Second, fair lending exposure: if you cannot see how decisions are made, you cannot verify protected characteristics are not being used as proxies. Third, model risk: problems are harder to detect without visibility into model behaviour. Fourth, customer harm: declined applicants given no explanation have no path back.

- How can lenders implement explainable AI without slowing down decision-making?

Modern XAI methods do not require a trade-off on speed. SHAP explanations for tree-based models — XGBoost, Random Forest — are generated in milliseconds as part of the same scoring call. The documentation and monitoring overhead sits offline. For real-time lending decisions, explainability adds negligible latency. The investment is in architecture and tooling, not in decision time.

Sources and Further Reading

- Lundberg, S.M. & Lee, S.I. (2017). A Unified Approach to Interpreting Model Predictions (SHAP). NeurIPS 2017. arxiv.org/abs/1705.07874

- Ribeiro, M.T. et al. (2016). 'Why Should I Trust You?': Explaining the Predictions of Any Classifier (LIME). KDD 2016. arxiv.org/abs/1602.04938

- European Parliament (2024). EU AI Act — Regulation 2024/1689. artificialintelligenceact.eu

- PRA (2023). Model Risk Management Principles for Banks (SS1/23). bankofengland.co.uk

- FCA (2022). Consumer Duty — Final Rules PS22/9. fca.org.uk

- Molnar, C. (2023). Interpretable Machine Learning, 3rd ed. christophm.github.io/interpretable-ml-book/

- British Business Bank (2023). SME Finance Survey 2023. british-business-bank.co.uk