Open Finance in Brazil: Transforming SME Lending with Data Access

Key Takeaways

|

Brazil’s open finance journey is no longer a regulatory experiment. It is the operating system of the country’s financial sector. In five years, the Banco Central do Brasil (“BCB”) has transformed a compliance mandate into a living infrastructure that connects banks, fintechs, insurers, and pension providers through standardised APIs and instant payments.[1] The tool, created by BCB for this is known as Pix[2] and may be analogous to Faster Payments in the UK or SEPA in the EU.

For lenders serving small and medium enterprises, the implications may be revelatory. Open finance in Brazil provides the data rails, payment channels, and regulatory clarity needed to assess credit risk with a precision that was impossible just three years ago.

This article examines how the ecosystem reached maturity, what it means for SME lending, and what open finance updates lenders should be preparing for in the rest of 2026 and beyond.

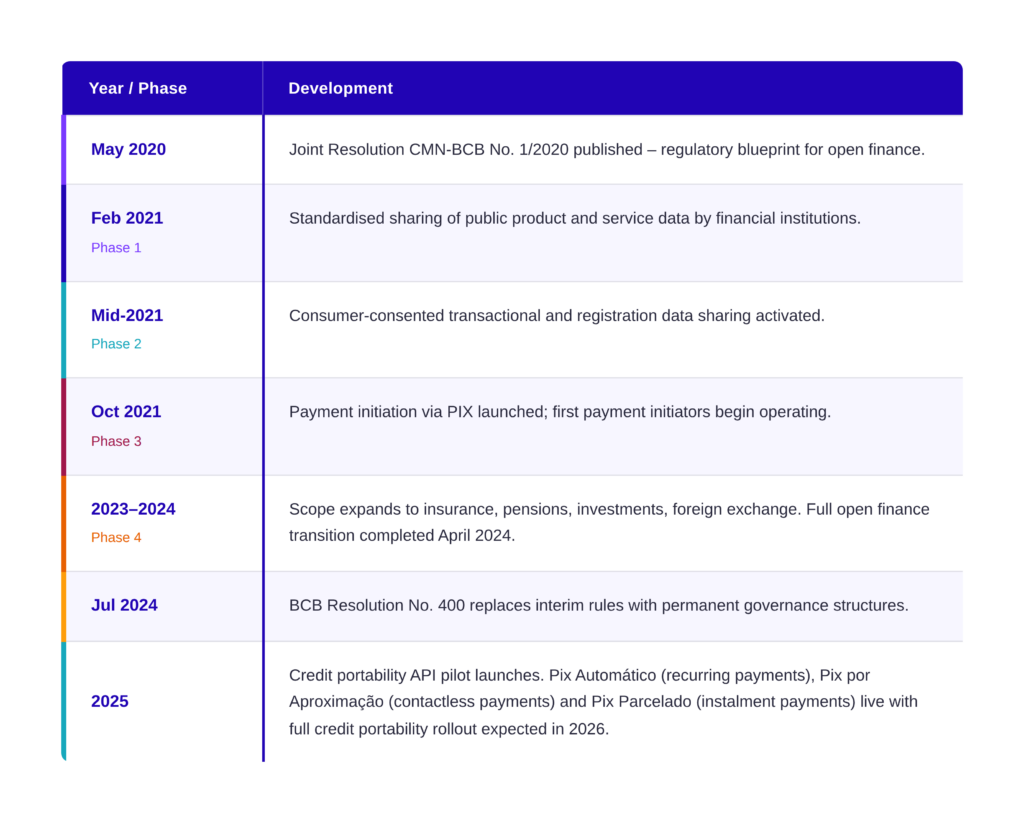

Brazil’s Five-Year Open Finance Journey Matures

When BCB published Joint Resolution CMN-BCB No. 1/2020 in May 2020, it laid out a phased blueprint for data sharing that went far beyond what most markets had attempted. Rather than limiting the scope to payment accounts, Brazil planned from the outset for a comprehensive open finance framework covering banking, insurance, pensions, investments, and foreign exchange.[3]

The four-phase rollout moved with remarkable speed:

- Phase 1 (February 2021) standardised public product data.

- Phase 2 (mid-2021) enabled consumer-consented transactional data sharing.

- Phase 3 (late 2021) introduced payment initiation through PIX.

- Phase 4 (from early 2023 through April 2024) completed the transition from open banking to open finance, integrating insurance, investment, and pension data into the unified ecosystem.[4]

As of 2026, the scale of the system is extraordinary.

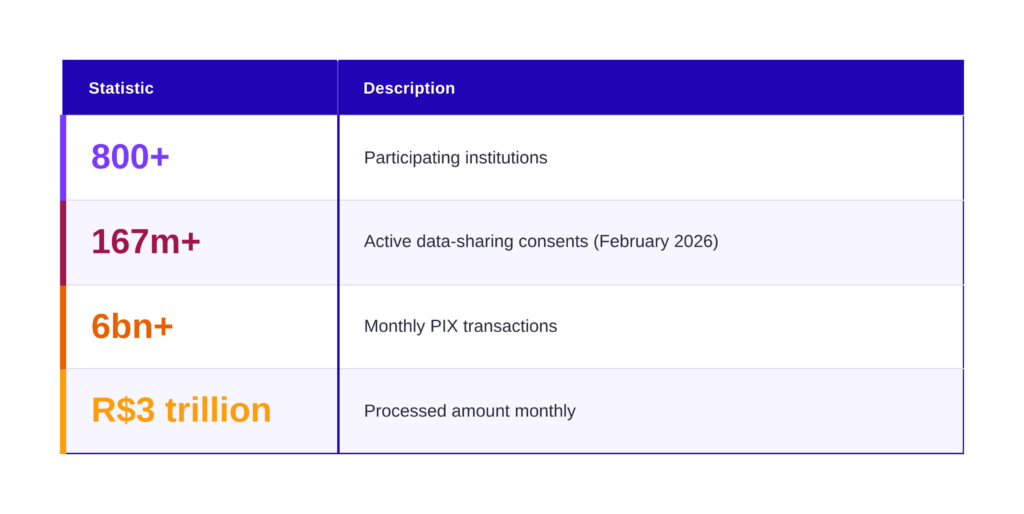

Open Finance Brasil accounts for more than 167 million active data-sharing authorisations[5] and Pix is estimated to be processing six to seven billion transactions per month in 2026 across more than 900 participating institutions.[6] In terms of value, Pix processes ~R$3 trillion per month (~US$557 billion), operating 24 hours a day, seven days a week and has a penetration rate that other open finance schemes might envy, reaching 91% of the Brazilian adult population, with 174 million natural persons in March 2026 and 22.3 million companies[7],2.

Timeline: Brazil’s Open Finance Implementation Phases (2020–2026)

Source: Banco Central do Brasil, Open Finance Brasil, Ozone API

How PIX Powers the World’s Largest Open Finance Ecosystem

PIX is not merely a payment system. It is the transactional backbone that transformed Brazil’s open finance framework from a data-sharing exercise into a functioning financial operating system.

Launched in November 2020 by the BCB, PIX enables real-time transfers 24/7 using a phone number, email, tax ID, or QR code. By December 2024, PIX was processing over 6 billion transactions per month, exceeding the combined volume of credit and debit card transactions by 80 per cent. On 20th December 2024, PIX set a single-day record of 252.1 million transactions.

The shift in transaction composition tells an important story for SME lenders. According to the BCB, by March 2025, 55 per cent of PIX transactions involved a business account, up from 38 per cent in February 2023.[8] This means PIX is increasingly generating the transactional data that open finance APIs can surface for credit assessment purposes.

The latest open finance Brazil news confirms several PIX enhancements in 2026:

- Pix Automático (automated recurring payments for subscriptions and utility bills),

- Pix por Aproximação (NFC contactless payments, introduced May 2025),

- Pix Parcelado (instalment payments accessing credit directly through PIX), and

- Pix em Garantia (enabling businesses to pledge future PIX receivables as collateral for credit).[9]

For lenders building on a core lending platform, PIX integration creates a continuous data stream. Rather than relying on a static credit application, lenders can observe how a business receives revenue, pays suppliers, manages seasonality, and handles cash-flow volatility – all in real time.

SME Credit Gap Meets Open Finance Solution

Brazil’s micro, small, and medium enterprises (MSMEs) constitute approximately 95 per cent of all businesses in the country, driving employment, innovation, and regional economic activity, and yet they have historically faced a financing gap estimated at $593 billion.[10]

The root causes are familiar: information asymmetry, collateral requirements that exclude asset-light businesses, concentrated banking markets that favour large corporates, and interest rates that remain punishingly high for smaller firms. OECD data shows Brazilian SMEs paying average interest rates of around 20.8 per cent per year, a figure that prices out many viable businesses from formal credit markets.[11]

Open finance in Brazil directly addresses the information asymmetry problem. With consented data sharing, a lender can access a business owner’s full financial footprint: transaction history across multiple banks, insurance coverage, investment positions, and pension arrangements. This is a step-change from the traditional model where a small business owner walks into a bank with a stack of paper statements and hopes for the best.

Research from Innovations for Poverty Action (IPA) conducted in Brazil’s Espírito Santo state confirms that PIX adoption among micro and small business owners is near-universal, at 96 per cent. However, only 15 per cent of those business owners had subscribed to open finance, and 65 per cent were unfamiliar with the concept. The opportunity, therefore, is not about technology readiness. The technology exists. The opportunity is about awareness, education, and product design that makes the value of data sharing tangible to SME owners.

Lenders pursuing digital transformation in lending can use open finance rails to build products that close this gap: pre-approved credit lines triggered by real-time revenue data, dynamic pricing that adjusts as a business’s financial profile changes, and onboarding flows that replace paperwork with consented API data pulls.

Credit Portability and Batch Payments Transform Business Lending

Amongst the most significant Brazilian open finance news developments for SME lenders is the launch of the Credit Portability API. This feature allows borrowers to transfer existing credit agreements between financial institutions entirely online, reducing the process from several weeks to as few as five days.[12]

The Credit Portability API entered its production pilot phase in November 2025 with 26 leading financial institutions participating. Initially focused on unsecured personal loans, the feature is expected to expand to other credit products. The broader market launch is scheduled for February 2026.[13] Open Finance Brasil has positioned credit portability as the flagship deliverable for the 2025–2026 period.

For SME lenders, credit portability changes the competitive landscape. A lender with superior data analytics and pricing models can now actively attract borrowers from incumbents by offering demonstrably better terms. The friction that previously locked borrowers into sub-optimal deals is being systematically removed.

Batch payments represent another critical development. As noted in recent open finance Brazil updates, SMEs are expected to play a larger role in the ecosystem as batch payment capabilities and tailored credit solutions mature. For businesses managing payroll, supplier payments, and recurring operational costs, batch PIX payments integrated through open finance APIs reduce administrative overhead and create cleaner transaction data for lenders to assess.

Lenders leveraging embedded lending capabilities within platforms can combine batch payments with working capital products, offering SMEs credit precisely when and where they need it – at the point of supplier payment or payroll processing.

From Consent Barriers to Mainstream Adoption

The early years of open banking Brazil news coverage were dominated by scepticism about consumer willingness to share data. The complaint was that users were granting consent without seeing tangible benefits – what industry observers called “consent for consent’s sake.”

That phase is over. The combination of consent-based data sharing and payment initiation now powers real products: Pix-by-proximity payments, buy-now-pay-later embedded in PIX, intelligent account sweeping, and recurring payments via Pix Automático. These innovations have moved beyond pilot stage into mainstream adoption.

The consent growth figures tell the story. Active consents grew 44 per cent year-on-year, from 43 million in January 2024 to 62 million in January 2025. By mid-2025, the number exceeded 100 million. The “Journey Without Redirection” initiative is further reducing friction by enabling payments to be initiated directly within merchant apps, eliminating the need to switch to a banking app.[14]

It may be instructive here to compare adoption rates between Brazil, the UK and EU: the UK has ~15 million[15] users of open banking in one form or another (e.g., consumers or businesses) as of 2025, equating to around 25% of the economically active population; by contrast, the EU rate is around 16%, although changes to EU legislation later in 2026 may increase this[16].

Brazil’s financial inclusion rate has climbed to 82 per cent among adults, up from 70 per cent in 2020, driven significantly by PIX and open finance infrastructure.[17] For lenders, rising consent rates mean a growing pool of potential borrowers whose financial data is accessible through standardised APIs – reducing acquisition costs and improving credit decisioning accuracy.

AI and Alternative Data Re-Shape Credit Decisions

Open finance provides the data. Artificial intelligence provides the analytical engine. Together, they are reshaping how credit decisions are made for Brazilian SMEs.

Brazilian fintechs are increasingly using alternative data – digital footprints, utility payment histories, device metadata, and social behaviour signals – to underwrite credit for thin-file or underserved borrowers.[18] When combined with open finance transaction data, these signals create a multi-dimensional credit profile that traditional bureau scores cannot match.

Comparison: Traditional Lending vs. PIX-Enabled Open Finance Credit Assessment

The Brazilian alternative lending market is projected to reach approximately $1.90 billion by 2025, with CAGR of ~14.3%. Embedded lending – where credit products are integrated into e-commerce, marketplace, and SaaS platforms – is becoming a dominant origination model, particularly for SME and consumer credit in digital commerce.

Lenders building on cloud lending architecture are best positioned to ingest these diverse data sources, run machine-learning models at scale, and deliver credit decisions in the timeframes that digitally-native SMEs expect.

The Road Ahead: 2026 and Onwards Regulatory Evolution

The regulatory pipeline for open finance Brazil updates in 2025–2026 is dense and consequential. Several developments deserve close attention from lenders.

Credit portability full rollout is expected to continue through 2026, following the November 2025 pilot. Pix accreditation requirements will formalise participation rules: non-authorised payment institutions must apply for BCB accreditation between January and May 2026.[19]

New cybersecurity and risk management requirements under BCB Resolution No. 522 (November 2025) expand risk categories for payment schemes to include financial, operational, AML/CFT, fraud, and ESG risks.[20] Brazil’s data protection law (LGPD, modelled on GDPR) is being actively enforced, with implications for how fintechs and lenders collect, store, and share customer data.

The BCB’s agenda also includes advancement of Drex (the Brazilian CBDC), Banking-as-a-Service regulation (following Public Consultation 108/2024), and virtual asset service provider (VASP) licensing from February 2026. Each of these will create new intersection points with the open finance ecosystem.

For lenders, the message is clear. The regulatory infrastructure is not only in place but actively evolving. Those who build now – integrating open finance data feeds, PIX payment rails, and AI-driven decisioning – will be positioned to capture market share as credit portability, batch payments, and new PIX features go live. Those who wait will find themselves competing against incumbents and fintechs that have already moved.

| ezbob Open Finance Integrationezbob’s platform provides pre-built integrations with open banking and open finance aggregators, configurable transaction analytics for credit risk, and consent management architecture designed for LGPD compliance and ongoing portfolio monitoring. Available via SaaS to banks and non-bank lenders. Contact us at ezbob.com/contact to discuss your open finance roadmap. |

Frequently Asked Questions

- What is Open Finance in Brazil and how does it differ from Open Banking?

Open Finance in Brazil extends the open banking framework beyond payment and current account data to cover insurance, pensions, investments, and foreign exchange. While open banking provides access to transaction history and balances from bank accounts, open finance gives consented access to a borrower’s complete financial life. For lenders, this means richer credit assessment using data from across the entire financial ecosystem, not just a single current account.

- How does PIX integrate with Brazil’s Open Finance ecosystem?

PIX is the instant payment infrastructure that underpins open finance’s transactional capabilities. Open Finance APIs allow third-party providers to initiate PIX payments on a customer’s behalf and access PIX transaction data for credit assessment. New features such as Pix Automático, Pix Parcelado, and Pix em Garantia are further integrating payments and lending, enabling recurring payments, instalment credit via PIX, and the use of PIX receivables as loan collateral.

- What is the SME financing gap in Brazil and how can Open Finance help?

Brazil’s MSME financing gap is estimated at $593 billion, driven by information asymmetry, high interest rates, collateral requirements, and banking market concentration. Open finance helps by replacing collateral-dependent models with real-time, data-driven credit assessment. Lenders can access consented transaction data across multiple banks, verify income through PIX flows, and build multi-dimensional risk profiles that make lending to previously underserved SMEs commercially viable.

- How does credit portability work under Brazil’s Open Finance framework?

The Credit Portability API enables borrowers to transfer existing credit agreements between financial institutions fully online, reducing the process to as few as five days. A proposing institution receives the borrower’s request, evaluates the existing contract terms via the API, and makes a competing offer. Settlement occurs through Brazil’s Reserve Transfer System. The pilot launched in November 2025 with 26 institutions, and full market rollout is expected by February 2026.

- What are the main regulatory updates for Open Finance Brazil in 2025–2026?

Key regulatory developments include the credit portability full rollout (February 2026), mandatory PIX accreditation for non-authorised payment institutions (January–May 2026), BCB Resolution No. 522 expanding risk management requirements, active LGPD enforcement for data handling, Banking-as-a-Service regulation under Public Consultation 108/2024, and VASP licensing from February 2026. The BCB is also advancing Drex, Brazil’s CBDC project.

Sources and Further Reading

- Banco Central do Brasil (2020). Joint Resolution CMN-BCB No. 1/2020. bcb.gov.br

- Ozone API (2025). The History of Open Finance in Brazil. ozoneapi.com

- LUXHUB (2025). An Open Banking (and Open Finance) Transformation in Brazil. luxhub.com

- IPA (2025). What Brazil’s Micro and Small Businesses Reveal About the Future of Digital Finance. poverty-action.org

- The Paypers (2025). Brazil’s Open Finance: Five Years of Evolution. thepaypers.com

- Raidiam (2025). How Credit Portability in Brazil is Unlocking Market Competitiveness. raidiam.com

- Taktile (2025). Brazil’s Top 25 of 2025: The Innovators Reshaping Financial Services. taktile.com

- Chambers and Partners (2025). Financial Services Regulation 2025 – Brazil. practiceguides.chambers.com

- ANBC (2025). Five Years of Open Finance. anbc.org.br

- The Banking Scene (2025). Lessons in Progress: Open Finance Around the World.thebankingscene.com

[1]Ozone API, “The History of Open Finance in Brazil,” October 2025. https://ozoneapi.com/blog/the-history-of-open-finance-in-brazil/

[2]LUXHUB, “An Open Banking (and Open Finance) Transformation in Brazil,” June 2025. https://luxhub.com/from-regulation-to-revolution-brazil-open-banking-finance-transformation/

[3] https://dashboard.openfinancebrasil.org.br/transactional-data/active-consents/receivers, 27 February 2026

[4]The Paypers, “Brazil’s Open Finance: Five Years of Evolution,” December 2025. https://thepaypers.com/fintech/expert-views/brazils-open-finance-five-years-of-evolution-and-ecosystem-building

[5] https://financialit.net/news/payments/pix-five-years-how-brazil-built-one-worlds-most-advanced-public-payments

[6]IPA / Innovations for Poverty Action, “What Brazil’s Micro and Small Businesses Reveal About the Future of Digital Finance,” 2025. https://poverty-action.org/what-brazils-micro-and-small-businesses-reveal-about-future-digital-finance

[7]Chambers and Partners, “Financial Services Regulation 2025 – Brazil: Trends and Developments,” 2025. https://practiceguides.chambers.com/practice-guides/financial-services-regulation-2025/brazil/trends-and-developments

[8]fundsforNGOs “Bridging Brazil’s $593B MSME Financing Gap,” May 2025. https://news.fundsforngos.org/2025/05/15/bridging-brazils-593b-msme-financing-gap-a-call-for-inclusive-growth/

[9]Springer, “The Financing of Small and Medium-Sized Enterprises: An Analysis of the Financing Gap in Brazil,” European Business Organization Law Review, 2019. https://link.springer.com/article/10.1007/s40804-019-00167-7

[10]Raidiam Developers, “How Open Finance Brasil’s Credit Portability API Works,” November 2025. https://www.raidiam.com/developers/blog/how-open-finance-brasil-credit-portability-api-works

[11]Raidiam, “How Credit Portability in Brazil is Unlocking Market Competitiveness,” December 2025. https://www.raidiam.com/insights/how-credit-portability-in-brazil-is-unlocking-market-competitiveness-with-open-finance

[12]Adyen, “PIX via Open Finance: Fewer Steps, More Conversion,” July 2025. https://www.adyen.com/the-latest/pix-via-open-finance-fewer-steps-more-conversion

[13] https://www.openbanking.org.uk/news/open-banking-surges-to-15-million-uk-users-as-july-marks-record-adoption

[14] https://finance.ec.europa.eu/publications/financial-data-access-and-payments-package_en

[15]BIIA, “Open Finance Enables Brazilian Consumers by Reshaping How They Leverage Financial Data – BCB Insights,” October 2025. https://www.biia.com/open-finance-enables-brazilian-consumers-by-reshaping-how-they-leverage-financial-data-bcb-insights/

[16]Taktile, “Brazil’s Top 25 of 2025: The Innovators Reshaping Financial Services,” November 2025. https://taktile.com/articles/brazil-top-25-of-2025

[17]Rio Times Online, “Brazil Fintech in 2026: Pix, Nubank, Open Finance and the Digital Banking Revolution,” March 2026. https://www.riotimesonline.com/brazil-fintech-2026-complete-guide/