How to Overcome Vendor Lock-In Without Building In-House

Key Takeaways

- Vendor lock-in risk can be mitigated through API-first architecture, open standards, and strategic contract negotiations without requiring expensive in-house development

- A composable, multi-vendor approach balances flexibility with operational efficiency, reducing complexity while preserving switching options

- Financial institutions must negotiate exit clauses, data portability requirements, and API access guarantees into vendor agreements from day one

Financial services organisations face a critical dilemma: how to adopt modern lending technology without sacrificing flexibility or independence. The threat of vendor lock-in looms large for banks and fintech companies evaluating their technology stack. Whether you’re using cloud infrastructure, lending platforms, or core banking systems, the fear that switching providers will become prohibitively expensive or impossible often paralyses decision-making.

The traditional answer has been to build everything in-house, but that comes with staggering costs, extended timelines, and ongoing maintenance burdens. This article explores a third path: how to avoid vendor lock-in risk through strategic architecture decisions, smart contract negotiations, and a pragmatic approach to platform selection without the overhead of in-house development.

Understanding Vendor Lock-In in Financial Services

Vendor lock-in occurs when the cost, difficulty, or technical barriers of switching to a competitor become so high that an organization effectively has no choice but to continue using an incumbent vendor, even if better or cheaper alternatives exist.

In financial services, this manifests in multiple ways:

- Proprietary data formats that cannot be easily exported or migrated to competing platforms

- Custom integrations built specifically for one vendors APIs that don’t work elsewhere

- Lack of data portability or punitive contract terms that make exit economically unfeasible

- Switching costs that include migration fees, consulting expenses, and operational disruption

For financial institutions managing customer deposits, loan portfolios, and regulatory compliance, vendor lock-in also creates strategic risk: you lose negotiating leverage on pricing, feature development priorities, and support responsiveness. The vendor knows you can’t leave, and that changes the power dynamic.

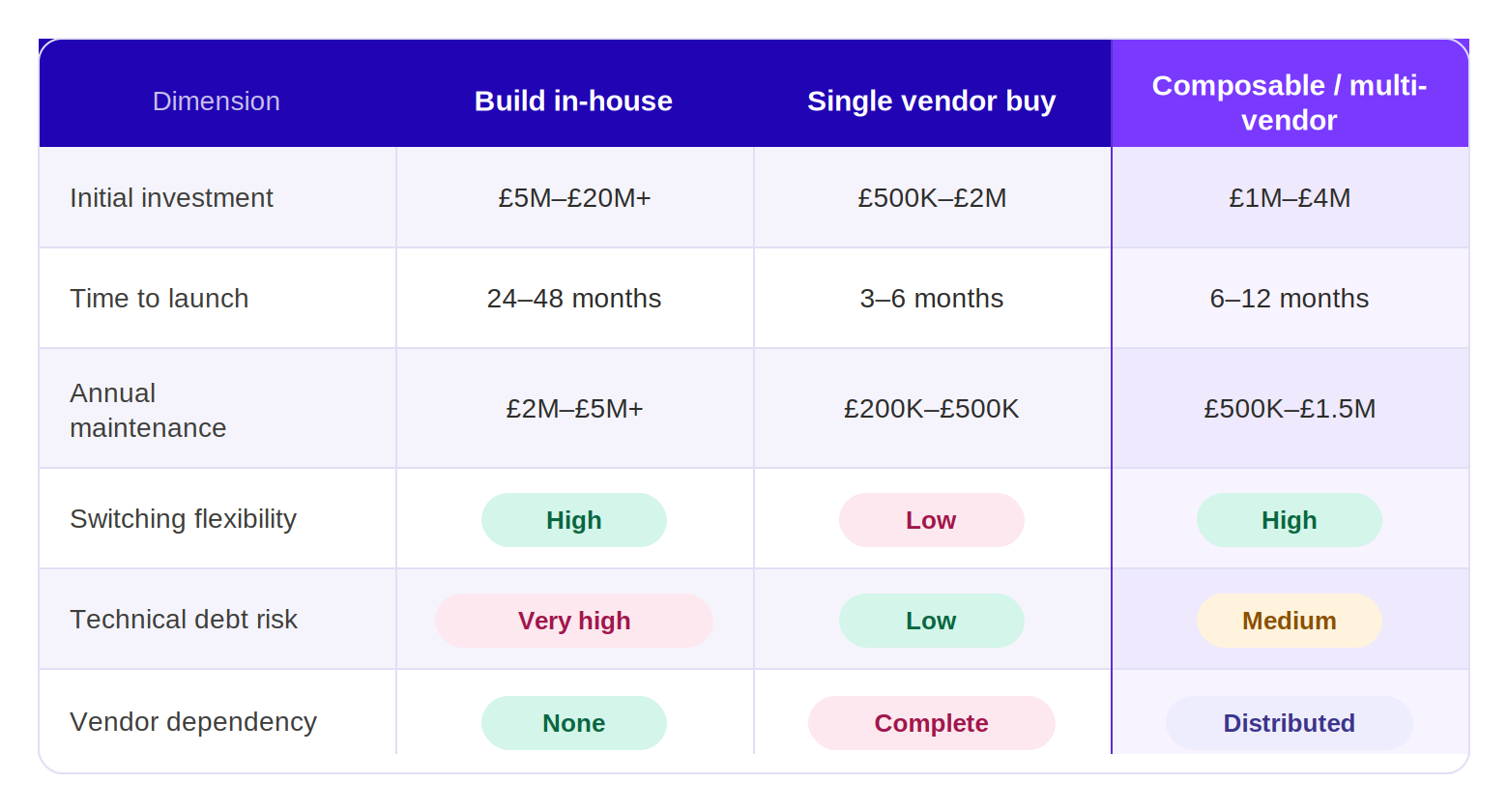

The Hidden Costs of Building vs. Buying Lending Technology

When faced with vendor lock-in concerns, many organizations consider building technology in-house. Before committing to that path, understand the true economics:

The temptation to build in-house is driven by the fear of supplier lock in. But in-house development creates its own lock-in - the lock-in of technical debt, staff retention risk, and the ongoing cost of innovation. Your team becomes locked into maintaining aging systems rather than focusing on competitive advantages.

The third column composable architecture with multiple vendors offers a pragmatic middle ground that deserves serious consideration.

API-First Architecture: Your Path to Platform Independence

Modern lending platforms succeed by adopting an API-first philosophy: every capability should be accessible through clearly defined, standards-based APIs. This architectural choice is the foundation for avoiding vendor lock-in.

An API-first approach means:

- Integrations don’t depend on proprietary SDKs or closed frameworks

- Your applications interact with vendor systems through standard REST, gRPC, or webhook interfaces

- Data models are transparent, enabling data portability and comparison between vendors

- Testing and development can proceed independently of vendor infrastructure

When evaluating vendors, demand comprehensive API documentation, SDKs in widely-used languages, and commitment to backward compatibility. Test integrations early in your evaluation. If a vendor resists API-first thinking or insists on proprietary tooling, that’s a red flag for potential lock-in.

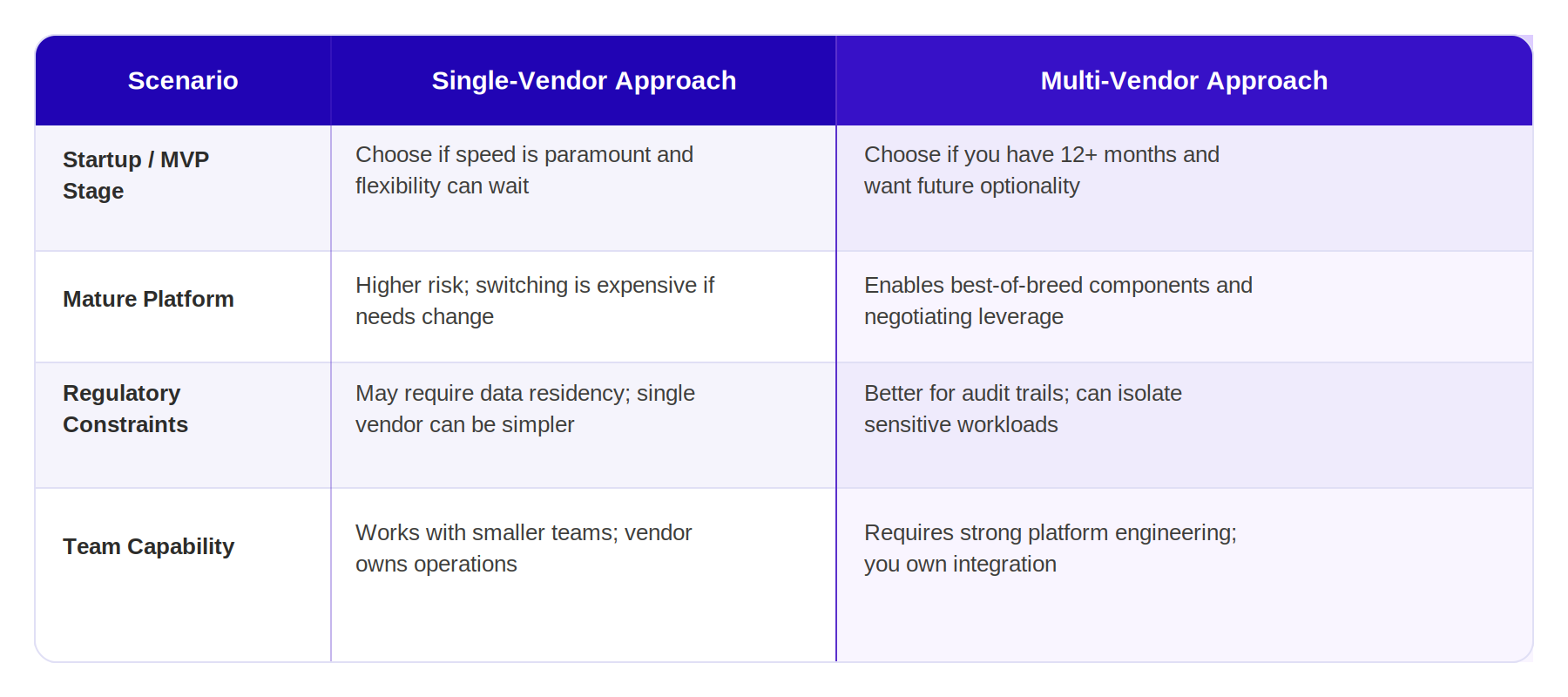

Decision Framework: Single-Vendor vs. Multi-Vendor

Different situations call for different approaches. Use this framework to evaluate what’s right for your organisation:

Open Standards and Interoperability in Banking Systems

The financial services industry is moving toward standardisation. Leverage this momentum. Standards like Open Banking (PSD2 in Europe, Open Banking in the UK) and emerging initiatives around composable banking create ecosystem effects that make switching easier and cheaper.

When evaluating best database software for avoiding vendor lock-in, or selecting any lending technology, ask:

- Does this platform support industry-standard APIs (e.g., Open Banking, loan origination standards)?

- Can you export customer data in standardized formats (CSV, JSON, or industry schemas)?

- Does the vendor participate in industry consortia or standards bodies?

- Are there established migration paths or partnerships with competitors?

Contract Negotiation Strategies That Preserve Flexibility

Your vendor contract is the legal foundation for your exit options. Default terms heavily favour the vendor; you must negotiate intentionally.

Key Contract Terms Checklist

- Data Ownership & Portability: Explicit language confirming you own all data and can export in standard formats within 30 days of termination

- API Access: Guaranteed access to all APIs during the contract term with 180-day notice before deprecation

- Exit Assistance: Vendor commits to 90-day migration support at documented rates; no penalties for consulting assistance

- Non-Disparagement Clause: Mutual agreement not to penalize customer for leaving or moving to competitor infrastructure

- Escrow for Source Code: For mission-critical systems, negotiate access to source code upon vendor bankruptcy

- Interoperability Roadmap: Commitment to maintain and improve API standards over the contract term

- Price Escalation Caps: Limit annual price increases to prevent lock-in through cost inflation (e.g., CPI + 2%)

Successful contracts create mutual incentives: the vendor wins your continued business through good service, not because leaving is impossible.

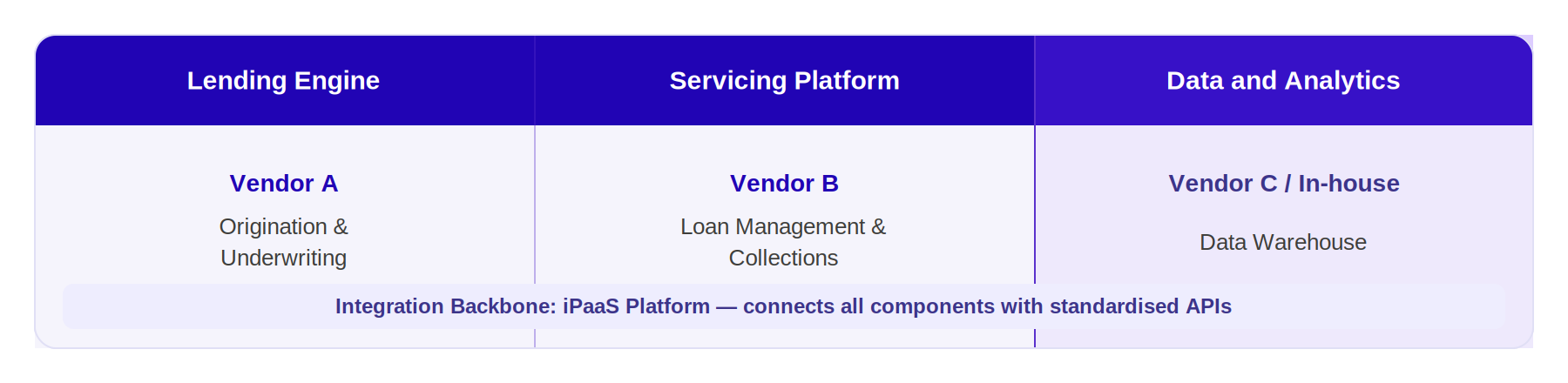

Multi-Vendor Architecture Without Complexity Overhead

The fear that a multi-vendor architecture creates complexity is valid but it’s manageable with the right approach. Consider this layered structure:

- Core lending engine: One vendor for origination and underwriting (your most critical path)

- Servicing platform: Second vendor for loan management and collections (separable, frequently upgraded)

- Data & analytics: Separate vendor or in-house (cloud data warehouse approach)

- Integration layer: iPaaS (integration-as-a-service) platform as the backbone

This layered approach reduces vendor lock-in cloud computing concerns while maintaining operational simplicity. If one vendor fails to innovate or increases prices aggressively, you can replace that layer without rebuilding your entire system.

Exit Planning: Building Portability from Day One

True protection against vendor lock-in comes from planning your exit before you’ve even signed on. Design your architecture with exit in mind:

- Conduct a migration simulation 12 months before contract renewal, identifying actual switching costs and time requirements

- Maintain a data export playbook documenting exactly which data lives where and how to retrieve it

- Build integration tests that verify data consistency between systems; they'll catch integration drift before migration

- Establish a vendor evaluation cadence (every 18 months) comparing your current vendor to alternatives

When contract renewal time arrives, you'll have real data on switching costs and realistic alternatives. That puts genuine negotiating leverage back in your hands.

Frequently Asked Questions

What is vendor lock-in and why is it a risk for banks?

Vendor lock-in occurs when switching costs (financial, technical, or operational) become so high that an organization has little practical choice but to continue with an incumbent vendor. For banks, this creates strategic risk: loss of negotiating leverage on pricing, reduced ability to adopt better technology, and dependency on a single vendors roadmap and support. It can also limit your ability to respond to market changes or regulatory requirements.

How can financial institutions avoid vendor lock-in without building in-house?

Focus on architecture decisions, not build decisions. Choose API-first vendors, negotiate contracts that guarantee data portability and API access, distribute critical functions across multiple vendors, and adopt open standards. Design your system so that replacing one vendor layer doesn’t require rewriting everything else. This approach preserves flexibility while leveraging vendors; speed and expertise.

What role do open APIs play in preventing vendor lock-in?

Open APIs are the technical foundation for portability. They enable your applications to communicate with vendor systems using standard protocols, not proprietary frameworks. If a vendor uses open REST APIs and standard data formats, switching to a competitor becomes a matter of repointing integrations, not rebuilding them. Vendors providing open APIs also tend to compete on innovation and service quality rather than lock-in tactics.

What contract terms should banks negotiate to reduce vendor lock-in risk?

Prioritize data ownership and portability, guaranteed API access with advance notice of deprecations, exit assistance clauses (vendor commits to migration support), escrow arrangements for critical source code, price escalation caps to prevent lock-in through cost inflation, and explicit rights to export customer data in standard formats. These terms shift the power dynamic, making the vendors continued success dependent on service quality rather than customer dependence.

How do best-of-breed solutions compare to single-vendor platforms?

Single-vendor platforms offer simplicity and integrated workflows but increase lock-in risk and limit flexibility. Best-of-breed solutions let you choose the best tool for each layer (origination, servicing, analytics) and switch components independently but require stronger integration capabilities. For mature financial institutions with sophisticated teams, best-of-breed approaches typically offer better long-term ROI and strategic flexibility, even though they demand more operational attention.

Conclusion

Vendor lock-in is not inevitable. It's a choice usually an implicit one made through default contract acceptance and architecture decisions made without exit planning. Financial institutions can preserve flexibility, negotiate better terms, and maintain strategic independence by adopting API-first thinking, negotiating intentionally, distributing critical functions across vendors, and planning for portability from day one.

This doesn’t mean avoiding vendor solutions. It means choosing vendors as strategic partners, not eternal masters. The institutions that thrive will be those that balance the speed and innovation that vendors provide with the flexibility and independence that only thoughtful architecture and negotiation can secure.

For more on building composable financial platforms that avoid vendor dependencies, explore composable banking architecture and the latest lending industry evolution.