Replacing Legacy Lending Systems with a Core Lending Platform

Key Takeaways

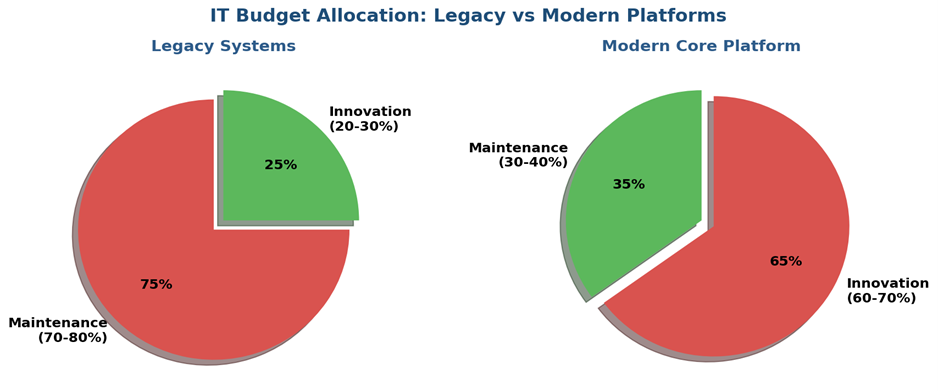

- Legacy lending systems create operational bottlenecks through manual processes, siloed data architectures, and limited API connectivity that prevent institutions from competing effectively in digital-first markets. Research indicates that financial institutions operating legacy systems allocate 70-80% of technology budgets to maintenance rather than innovation.1

- Modern core lending platforms enable end-to-end automation from origination through servicing, with cloud-native architectures that support real-time decisioning, embedded finance partnerships, and regulatory compliance at scale. Industry studies show that institutions implementing modern platforms achieve 40-60% reductions in loan origination costs and 30-50% improvements in staff productivity.2

- Strategic data migration is the critical success factor in platform replacement, requiring comprehensive field mapping, validation frameworks, and parallel running periods to ensure business continuity whilst unlocking the value of historical lending data. According to Gartner, 83% of data migration projects either exceed budget or fail entirely due to inadequate planning.3

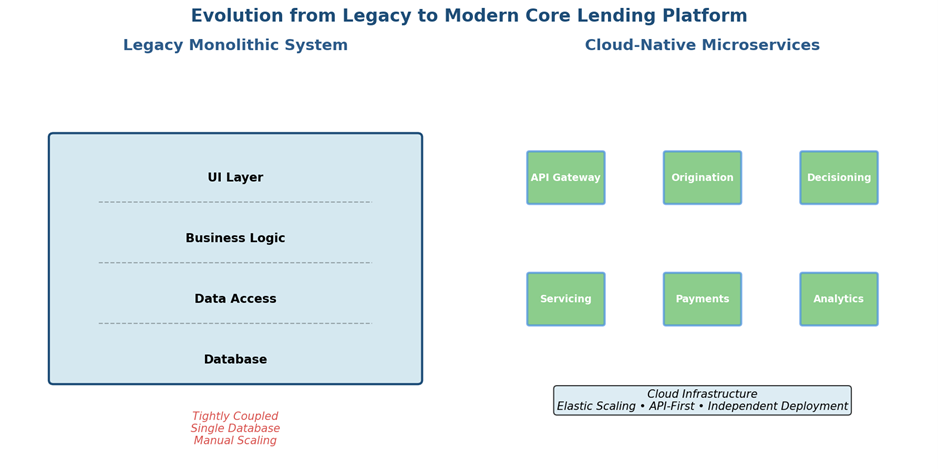

Figure 1: Evolution from Legacy Monolith to Cloud-Native

Introduction

The financial services industry stands at an inflection point. Institutions running loan portfolios on systems built in the 1990s and early 2000s face mounting pressure from digital-native competitors, evolving regulatory requirements, and customer expectations shaped by seamless consumer technology experiences. The gap between what legacy lending systems can deliver and what modern markets demand has become a strategic liability.

For many banks and specialist lenders, the question is no longer whether to replace legacy infrastructure, but how to execute a transformation that minimises risk whilst maximising the operational and competitive benefits of a modern core lending platform.

Why Legacy Lending Systems Are Holding Institutions Back

Legacy lending systems were purpose-built for a different era of financial services. Many of these platforms emerged when lending was primarily branch-based, regulatory reporting requirements were less complex, and the concept of real-time credit decisioning was purely theoretical.

Today, these same systems create fundamental constraints on institutional competitiveness.

Technical Debt and Maintenance Burden

Institutions operating legacy loan management systems typically allocate 70-80% of their technology budgets to maintenance rather than innovation.4

Ageing codebases written in languages like COBOL or early Java frameworks require increasingly scarce specialist talent and a recent survey found that 43% of banking executives cite 'inability to find qualified talent for legacy systems' as their primary technical constraint.5 Whilst this is a problem we know about from NASA in maintaining satellites like the Voyager probes as they leave the solar system, it’s a problem for modern bank CTOs also.

Custom modifications accumulated over decades often create brittle architectures where seemingly simple changes can have unpredictable downstream effects across loan origination, decisioning, and servicing functions.

Data Architecture Limitations

Legacy systems were designed around relational database structures optimised for transaction processing rather than analytics. Customer data, lending data, and risk data often exist in separate siloes with limited integration capabilities.

McKinsey research indicates that financial institutions with siloed legacy systems experience 35% higher operational costs and 23% lower customer satisfaction scores compared to those with unified data platforms.6

This fragmentation makes it extremely difficult to generate the 360° customer views required for effective relationship banking or to feed the machine learning models that power modern credit decisioning.

API and Integration Constraints

The shift towards open banking, embedded finance, and platform-based business models demands extensive API connectivity. Legacy lending systems typically lack native RESTful API frameworks, forcing institutions to build complex middleware layers to connect with third-party data providers, credit bureaux, fraud detection services, and partner distribution channels. Each integration becomes a custom development project rather than a configuration exercise. Industry analysis suggests that API-first platforms reduce integration costs by 60% and time-to-market for new partnerships by 75%.7

Figure 2: IT Budget Allocation - Comparing Legacy to Modern

Regulatory and Compliance Challenges

Modern regulatory frameworks—whether FCA requirements in the UK, CECL standards in the US, or IFRS 9 globally—demand granular data capture, sophisticated expected credit loss modelling, and comprehensive audit trails.

Legacy loan management systems often require expensive bolt-on solutions to meet these requirements, creating parallel data structures and reconciliation challenges that increase operational risk. The Bank of England estimates that UK banks spend £4-5 billion annually on regulatory compliance, with legacy system constraints accounting for approximately 40% of these costs.8

Customer Experience Constraints

In an era where consumers expect instant credit decisions and seamless digital experiences, legacy systems create bottlenecks. Manual processes, batch-based decision engines, and limited self-service capabilities result in application abandonment rates that can exceed 40% for digital channels.9

The inability to support real-time affordability assessments or dynamic pricing based on relationship data represents a direct competitive disadvantage. Research from Accenture found that 57% of consumers would switch financial providers for better digital experiences.10

What Is a Core Lending Platform and How Does It Differ from Legacy LMS/LOS?

Understanding the architectural and functional differences between legacy systems and modern core lending platforms is essential for evaluating transformation opportunities.

Architectural Foundation

Traditional loan management systems and loan origination systems were typically built as monolithic applications with tightly coupled components. A modern core lending platform employs microservices architecture, containerisation, and cloud-native design principles that enable independent scaling, deployment, and updates of individual components without system-wide downtime.

This fundamental architectural shift delivers several critical advantages:

- Elastic scalability: Cloud-based infrastructure that will automatically scale to handle application volume spikes during promotional campaigns or seasonal peaks without manual capacity planning

- Continuous deployment: Microservices enable frequent feature releases and regulatory updates without lengthy testing cycles for the entire application stack

- Resilience: Distributed architecture with automated failover capabilities ensures that component failures don't cascade into system-wide outages. AWS reports that cloud-native financial applications achieve 99.95% uptime compared to 99.5% for legacy, on-premises, systems: this 0.45% might sound small, but that’s an additional 39 hours 25 minutes 12 seconds of uptime per annum .11

End-to-End Process Coverage

Legacy environments typically separate origination and servicing functions across different systems, creating handoff points that require manual intervention and increase operational risk.

Core lending platforms by contrast provide unified coverage from initial customer enquiry through loan booking, draw-down, servicing, collections, and eventual settlement, with consistent data models and business rules across the entire lending lifecycle. Studies show this unified approach reduces loan processing time by 65% and error rates by 80%.12

Configurable Business Rules Engines

Rather than requiring developer intervention for each business rule change, modern platforms provide low-code or no-code configuration interfaces that enable business users to modify credit policies, pricing strategies, and workflow logic.

This dramatically reduces time-to-market for new products—from an average of 18 months with legacy systems to 6-8 weeks with modern platforms13—and enables rapid responses to competitive pressures or regulatory changes.

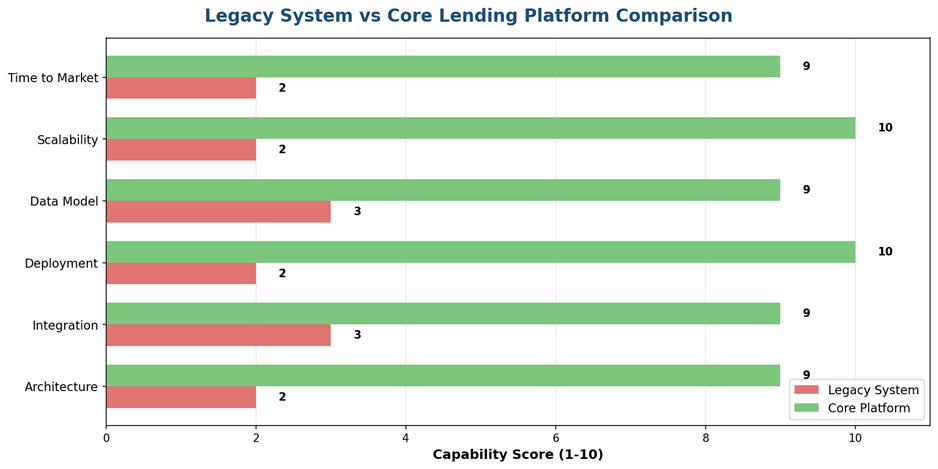

Figure 3: Capability Comparison, comparing Legacy and Modern Platforms

Native API-First Architecture

Core lending platforms expose comprehensive APIs for every core business function, enabling seamless connection with, for example, pre-built integrations to:

- Credit bureaux and alternative data providers for real-time decisioning (e.g., Open Banking)

- Fraud detection and identity verification services to meet CDD requirements

- Accounting systems for automated transaction posting, reconciliation and treasury

- Customer relationship management platforms such as Salesforce or similar

- Partner channels for embedded lending and financial product distribution

Advanced Analytics, ML and AI Integration

Modern platforms incorporate machine learning capabilities for credit risk assessment, fraud detection, customer segmentation, and behavioural analytics.

Rather than requiring data to be extracted, transformed, and loaded into separate analytics environments, these capabilities operate on live data within the lending platform itself.

The emergence of agentic AI in lending and financial services represents the next evolution, where autonomous agents can optimise decisioning workflows, identify portfolio risks, and recommend actions based on comprehensive pattern analysis. Early adopters report 28% improvements in credit decision accuracy and 35% reductions in fraud losses.14

Business and Technology Drivers for Replacing Legacy Lending Systems

The decision to replace core lending infrastructure represents one of the most significant technology investments a financial institution can make. Understanding the specific drivers helps build the business case and prioritise requirements.

Revenue Growth and Market Expansion

Legacy systems constrain product innovation and market responsiveness. Institutions find themselves unable to launch new lending products quickly enough to capitalise on market opportunities or respond to competitor offerings. A modern core lending platform enables:

- Rapid product configuration: Launch new loan products in days rather than quarters—Forrester research shows modern platforms reduce product launch cycles by 73%15

- Dynamic pricing optimisation: Implement risk-based pricing that balances portfolio performance with competitive positioning

- Embedded finance: Distribute lending products through third-party platforms, fintech partners, and non-financial brands—the embedded finance market is projected to reach £230 billion by 202616

- Geographic expansion: Configure jurisdiction-specific business rules and regulatory requirements without separate system implementations meaning that an EU-wide product could be offered for those businesses in multiple countries

Operational Efficiency and Cost Reduction

The total cost of ownership for legacy lending systems extends far beyond licence and maintenance fees. Hidden costs accumulate through manual processes, error correction, reconciliation overhead, and the opportunity cost of staff time spent on routine tasks rather than value-added activities. By contrast, those organisations replacing legacy infrastructure typically achieve:

- 40-60% reduction in loan origination costs through automated decisioning and document processing17

- 30-50% improvement in staff productivity through elimination of manual data entry and reconciliation tasks18

- Significant reduction in operational risk events related to manual errors or data inconsistencies—typically 65-75% fewer incidents

- Lower infrastructure costs through cloud economics that align spending with usage—organisations report 35-45% reduction in IT infrastructure costs19

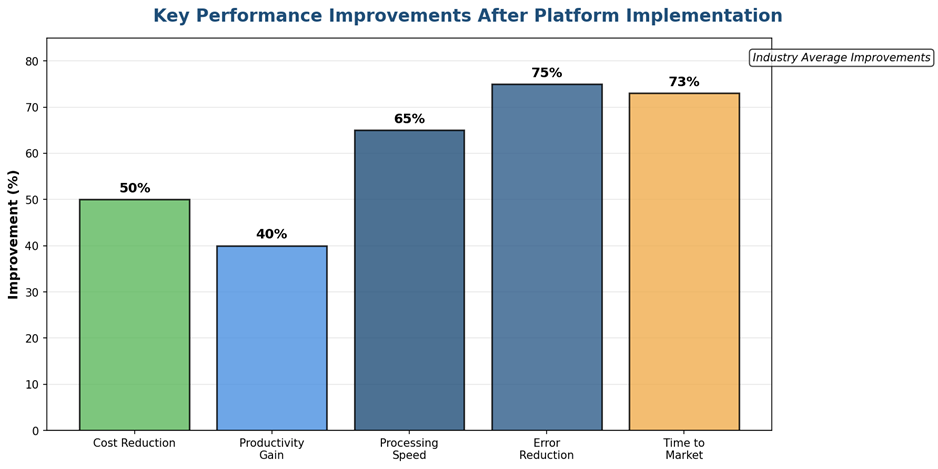

Figure 4: Industry Average Improvement in KPIs after Modern Platform Implementation

Regulatory Compliance and Risk Management

Regulatory requirements continue to evolve in complexity and scope, and legacy systems often struggle to adapt to, for example:

- Enhanced conduct risk requirements: FCA expectations for fair treatment of customers, vulnerable customer identification, and affordability assessments to include the relatively new Consumer Duty, which came into effect in 2023

- Financial crime prevention: Anti-money laundering, sanctions screening (as CDD) and fraud detection requirements that demand real-time data correlation

- Expected credit loss modelling: IFRS 9 and CECL standards requiring granular loan-level data and sophisticated forecasting capabilities to include identification of SICR triggers

- Operational resilience: Requirements for documented recovery time objectives and comprehensive testing of critical business services—the FCA's operational resilience regime requires important business services to remain within impact tolerances20

Modern core lending platforms embed these requirements into their operational frameworks rather than treating compliance as a bolt-on consideration.

Digital Transformation and Customer Experience

Customer expectations have fundamentally shifted, and borrowers expect:

- Instant credit decisions for straightforward applications, with >80% of consumers expecting decisions in minutes and hours, not days

- Mobile-first interfaces with biometric authentication – using face mapping on mobile devices

- Self-service account management and payment flexibility

- Transparent communication about application status and decisioning factors

- Personalised product recommendations based on relationship history

Legacy lending systems cannot deliver these experiences without extensive custom development that creates unsustainable technical debt over time.

Data-Driven Decision Making

Financial institutions increasingly compete on their ability to leverage data for strategic advantage.

Legacy systems imprison valuable lending data in formats that require complex extraction processes before analysis can occur. Modern platforms provide:

- Real-time dashboards for portfolio performance monitoring

- Predictive analytics of portfolio deterioration enabling proactive intervention 3-6 months earlier than reactive approaches – including CRM interventions for customers where financial difficulty is identified

- Customer behaviour insights that inform retention and cross-sell strategies

- A/B testing frameworks for optimising decisioning models and customer journeys—leading to 15-25% improvement in conversion rates21

Smart Data Migration: The Bridge Between Legacy and a Modern Core Lending Platform

Data migration represents the highest-risk element of any lending platform replacement initiative. The challenge isn't simply moving records from one database to another—it's ensuring that decades of lending history, customer relationships, and business context transfer accurately whilst maintaining operational continuity.

Comprehensive Data Assessment and Mapping

Successful migrations begin with forensic analysis of legacy data structures:

- Data quality audit: Identify inconsistencies, duplicates, orphaned records, and referential integrity violations that must be resolved before migration

- Field-level mapping: Document the semantic relationship between legacy and target fields, including data type conversions, calculation logic, and business rule dependencies

- Historical significance assessment: Determine which historical data must migrate to the new platform versus what can be archived for reference-only access

- Regulatory data requirements: Ensure loan-level data required for regulatory reporting, stress testing, and provisioning calculations transfers completely

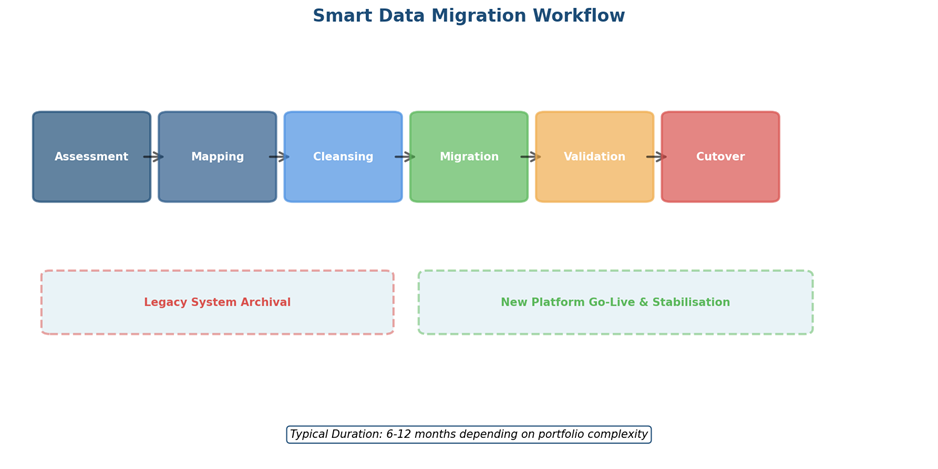

Organisations often discover that 20-30% of data in legacy systems is either duplicated, obsolete, or of questionable quality.22 Migration projects provide an opportunity for data cleansing that delivers long-term operational benefits: an example of this is as shown at figure five below.

Figure 5: Smart Data Migration Workflow (Example, showing parallel processing)

Migration Architecture and Tooling

Multiple technical approaches exist for data migration, each with specific risk profiles:

- Big Bang Migration: Complete cutover during a defined downtime window. This approach minimises the period during which dual systems operate but concentrates execution risk.

- Phased Migration: Migrate specific loan products, portfolios, or customer segments incrementally. This reduces single-point-of-failure risk but extends the period of operating parallel systems and requires careful management of cross-portfolio dependencies.

- Parallel Running: Maintain legacy and new systems simultaneously for a defined period, comparing outputs and reconciling discrepancies. This maximises confidence but doubles operational overhead during the transition period.

Most successful migrations employ hybrid approaches: parallel running for high-value or complex portfolios combined with phased cutover for simpler products. Industry data shows that phased approaches reduce migration failure risk by 60% compared to big bang implementations.23

Data Validation and Reconciliation

Validation frameworks must verify multiple dimensions:

- Structural validation: Confirm all records migrate with appropriate data types and referential integrity

- Calculation validation: Verify that interest accruals, payment allocations, and balance calculations produce identical results in both systems—typically requiring tolerance levels of ±£0.01 for rounding differences

- Regulatory validation: Ensure regulatory reporting extracts from the new platform match legacy outputs

- Business process validation: Confirm that servicing workflows, collection processes, and customer communications function correctly

Organisations should plan for multiple migration test cycles—typically 3-5 iterations—with each iteration improving data quality and validation comprehensiveness. Experience shows that organisations conducting fewer than 3 test cycles experience 3x higher post-migration defect rates.24

Managing Transactional Continuity

Lending businesses don't pause for technology migrations. The migration approach must account for:

- New loan applications being processed during migration periods

- Payment processing and allocation across both legacy and new systems

- Customer service requests that may reference data in either system

- Regulatory reporting deadlines that cannot accommodate migration delays

This typically requires temporary integration layers that synchronise data between systems during transition periods and comprehensive training programmes that enable staff to operate effectively in dual-system environments.

Historical Data Archival Strategy

Complete historical migration isn't always economically rational. For loans originated decades ago that have long since closed, maintaining full operational data in the new platform may not justify the migration complexity. A tiered approach often works best:

- Active loans: Full migration with complete transaction history

- Recently paid loans: Migration of summary data with detailed history archived—typically loans closed within the past 6-7 years to meet regulatory retention requirements

- Aged historical loans: Reference-only archival with read-only access for audit or customer enquiry purposes

Minimising Risk and Downtime During Lending System Replacement

Platform replacements fail not because of technology limitations but because of inadequate risk management, stakeholder preparation, and execution discipline.

Executive Sponsorship and Cross-Functional Governance

Lending platform replacements affect every area of the business. Success requires active sponsorship from C-suite executives who can:

- Make timely decisions when trade-offs arise between scope, timeline, and risk tolerance

- Allocate sufficient resources including dedicated business subject matter experts—typically 15-20% of key business users' time over 12-18 months

- Communicate transformation objectives and progress across the organisation

- Hold both internal teams and vendor partners accountable for delivery commitments

Governance structures should include representatives from lending operations, risk management, compliance, finance, IT, and customer service, ensuring that all perspectives inform critical decisions. Studies of successful transformations show that organisations with executive steering committees meeting fortnightly experience 45% fewer project delays than those with monthly governance.25

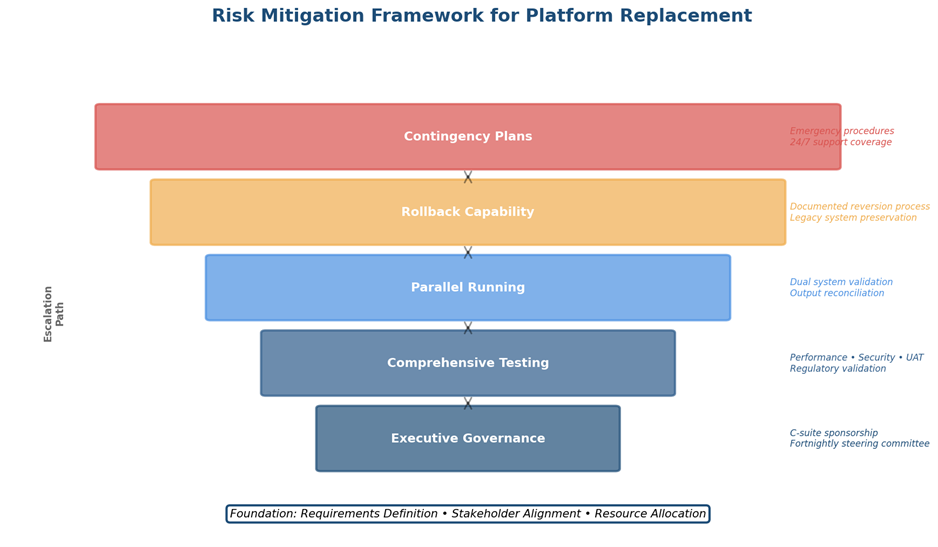

Figure 6: Example Risk Management Framework for Platform Replacement

Detailed Requirements Definition and Use Case Validation

Vague requirements lead to expensive scope creep and implementations that don't meet business needs. Requirements should be documented at three levels:

- Business capabilities: High-level outcomes the platform must enable (e.g., 'Support multi-currency lending with automated foreign exchange hedging')

- Functional requirements: Specific system behaviours (e.g., 'Calculate daily interest accrual using actual/365 day count convention')

- Non-functional requirements: Performance, scalability, security, and compliance standards—e.g., 'Process 10,000 loan applications per hour with <2 second response time at 95th percentile'

Each requirement should link to specific business use cases that can be validated through testing. Organisations with comprehensive requirements traceability experience 50% fewer post-implementation change requests.26

Comprehensive Testing Strategy

Testing must extend far beyond system integration testing:

- Unit testing: Verify individual components function correctly in isolation

- Integration testing: Confirm that integrated components produce expected results

- User acceptance testing: Validate that business users can execute complete workflows successfully

- Performance testing: Ensure the platform handles expected transaction volumes with acceptable response times—typically testing at 150% of projected peak load

- Resilience testing: Verify behaviour under failure scenarios including database unavailability, network disruptions, and third-party service outages

- Security testing: Conduct penetration testing and vulnerability assessments—OWASP Top 10 as minimum standard

- Regulatory testing: Validate all regulatory reporting outputs against known-good data sets

Institutions should allocate 30-40% of total project time to testing activities.27 Organisations that allocate less than 25% to testing experience 4x higher post-implementation defect rates.

Training and Change Management

Technology replacement requires operational changes that affect hundreds or thousands of staff members. Effective change management includes:

- Role-based training programmes: Different user populations (underwriters, servicing staff, collections agents) require tailored training

- Sandbox environments: Provide access to test systems where staff can experiment without fear of impacting production data

- Super-user networks: Identify and train power users within each business unit who can provide peer support during the transition—typically 1 super-user per 10-15 end users

- Documentation and job aids: Create reference materials that support day-to-day operations after formal training concludes

Contingency Planning and Rollback Capabilities

Despite comprehensive testing, production cutovers sometimes reveal issues that weren't apparent in pre-production environments. Contingency plans should address:

- Rollback procedures: Documented steps for reverting to legacy systems if critical issues emerge—with clear decision criteria for invoking rollback

- Data preservation: Ensure legacy data remains accessible if rollback becomes necessary—typically maintaining legacy environment in read-only mode for 90 days post-cutover

- Communication protocols: Pre-defined escalation paths and stakeholder communication procedures for managing incidents

- Extended support coverage: Ensure vendor and internal resources are available for extended periods following cutover to address issues rapidly—typically 24/7 coverage for first week, then extended hours for subsequent month

Frequently Asked Questions

What are the main risks of staying on a legacy lending system?

Institutions operating legacy lending systems face mounting operational, competitive, and regulatory risks. Technical debt constrains innovation capacity, with most IT budgets consumed by maintenance rather than strategic initiatives. Data siloes prevent effective risk management and customer relationship strategies. Limited API connectivity restricts participation in open banking and embedded finance ecosystems. Most critically, regulatory compliance becomes increasingly expensive and complex as modern frameworks demand data granularity and real-time capabilities that legacy architectures cannot support efficiently.

How does a core lending platform differ from a traditional loan management system?

Core lending platforms provide unified end-to-end functionality from origination through servicing, whereas traditional systems typically separate these functions. Modern platforms employ cloud-native microservices architectures enabling independent scaling and continuous deployment, compared to monolithic legacy structures. They offer configurable business rules engines that business users can modify without developer intervention, native API-first designs for seamless integration, and embedded analytics capabilities. Additionally, core platforms support modern lending models including embedded finance, dynamic pricing, and AI-driven decisioning that legacy systems cannot accommodate.

How can banks minimise downtime during lending system migration?

Minimising migration downtime requires sophisticated planning across multiple dimensions. Parallel running periods allow validation of new system outputs against legacy calculations before cutover. Phased migration approaches transition lower-risk portfolios first, building confidence before migrating complex products. Comprehensive testing strategies including performance, resilience, and user acceptance testing identify issues before production deployment. Organisations should establish detailed rollback procedures, maintain temporary integration layers for data synchronisation, and ensure executive sponsorship to enable rapid decision-making when challenges arise during transition periods.

What role does data migration play in successful core lending transformation?

Data migration represents the critical success factor in lending platform replacement, serving as the bridge between legacy operations and modern capabilities. Comprehensive field mapping ensures lending history, customer relationships, and regulatory data transfer accurately. Quality assessment and cleansing during migration eliminate inconsistencies that impair new platform performance. Multi-dimensional validation frameworks verify structural integrity, calculation accuracy, and regulatory reporting consistency. Strategic archival approaches balance completeness with migration complexity. Successful migrations preserve institutional knowledge embedded in historical data whilst unlocking analytical capabilities impossible within legacy constraints.

How do modern cloud-based lending platforms improve compliance and security?

Cloud-based lending platforms enhance compliance and security through multiple mechanisms. Automated regulatory reporting frameworks adapt to evolving requirements without custom development. Built-in audit trails provide comprehensive transaction histories for regulatory examination. Advanced encryption and tokenisation protect sensitive data both in transit and at rest. Continuous security monitoring and automated patch management reduce vulnerability windows. Cloud providers maintain extensive compliance certifications (SOC 2, ISO 27001, PCI-DSS) that individual institutions struggle to achieve independently. Additionally, cloud-native disaster recovery and business continuity capabilities that exceed legacy on-premises infrastructure can deliver economically.

Conclusion

The transformation from legacy lending systems to modern core lending platforms represents more than a technology upgrade—it's a fundamental reimagining of how financial institutions serve customers, manage risk, and compete in digital markets. Whilst the migration journey demands careful planning, executive commitment, and disciplined execution, the alternative—continuing to operate increasingly obsolete infrastructure—poses greater long-term risk to institutional viability.

Organisations that approach platform replacement with clear strategic objectives, comprehensive risk management frameworks, and appropriate investment in data migration capabilities position themselves not merely to preserve existing operations but to unlock new revenue opportunities, operational efficiencies, and customer experiences that legacy systems could never support.

The institutions that will thrive in the next decade of financial services are those making these transformations today.

About ezbob

ezbob provides cloud-native lending technology that enables financial institutions to replace legacy systems with modern, API-first platforms designed for digital transformation. Our comprehensive solutions support the entire lending lifecycle whilst minimising migration risk through proven data transformation frameworks and extensive regulatory compliance capabilities.

References

- Deloitte (2024). 'Banking Technology Trends: Legacy System Costs and Innovation Constraints'. Deloitte Insights.

- Celent (2023). 'Digital Lending Transformation: Operational Efficiency Gains from Platform Modernisation'. Celent Research.

- Gartner (2024). 'Data Migration Success Factors in Financial Services'. Gartner Research.

- McKinsey & Company (2023). 'The Cost of Legacy: Technology Debt in Financial Services'. McKinsey Digital.

- Accenture Banking Technology Vision (2024). 'Talent Challenges in Legacy System Maintenance'. Accenture Research.

- McKinsey & Company (2023). 'Data Unification and Customer Experience in Banking'. McKinsey Quarterly.

- Boston Consulting Group (2024). 'API-First Banking: Integration Cost Reduction Through Modern Architectures'. BCG Financial Services.

- Bank of England (2023). 'Regulatory Compliance Costs in UK Banking Sector'. Bank of England Quarterly Bulletin.

- Bain & Company (2024). 'Digital Lending: Application Abandonment Rates and Customer Journey Optimisation'. Bain Financial Services Report.

- Accenture (2023). 'Consumer Banking Experience Study: Digital Expectations and Switching Behaviour'. Accenture Consumer Research.

- Amazon Web Services (2024). 'Cloud-Native Financial Services: Uptime and Resilience Benchmarks'. AWS Financial Services Report.

- Capgemini (2023). 'Unified Lending Platforms: Efficiency Gains in Loan Processing'. Capgemini Financial Services Analysis.

- Forrester Research (2024). 'Low-Code Lending Platforms: Time-to-Market Reduction for Financial Products'. Forrester Wave Report.

- International Data Corporation (2024). 'AI in Lending: Performance Improvements in Credit Decisioning and Fraud Detection'. IDC Financial Insights.

- Forrester Research (2023). 'Digital Product Launch Velocity: Modern vs Legacy Platforms'. Forrester Total Economic Impact Study.

- Juniper Research (2024). 'Embedded Finance Market Projections 2024-2026'. Juniper Research Banking Report.

- PwC (2023). 'Digital Lending Transformation: Operational Cost Reduction Through Automation'. PwC Financial Services Technology.

- EY (2024). 'Lending Operations Productivity: Impact of Process Automation'. EY Financial Services Report.

- KPMG (2023). 'Cloud Economics in Banking: Infrastructure Cost Reduction Case Studies'. KPMG Global Banking Survey.

- Financial Conduct Authority (2022). 'Operational Resilience: Important Business Services Framework'. FCA Policy Statement PS21/3.

- Oliver Wyman (2024). 'Digital Lending Optimisation: A/B Testing and Conversion Rate Improvements'. Oliver Wyman Financial Services.

- IBM Institute for Business Value (2023). 'Data Quality in Legacy Systems: Migration Opportunities for Cleansing'. IBM Banking & Financial Markets Report.

- Everest Group (2024). 'Migration Strategy Risk Analysis: Big Bang vs Phased Approaches'. Everest Group Research.

- Cognizant (2023). 'Testing Rigour and Post-Implementation Defect Rates in System Migrations'. Cognizant Technology Solutions Report.

- Project Management Institute (2024). 'Governance Frequency and Project Delivery Success in Technology Transformations'. PMI Research.

- International Institute of Business Analysis (2023). 'Requirements Traceability Impact on Change Request Volumes'. IIBA Global Survey.

- CAST Software (2024). 'Testing Investment and Quality Outcomes in Enterprise Software Projects'. CAST Research Labs.