SME Lending in Africa: How Alternative Data Drives Credit Decisions

Key Takeaways

- Africa's SME financing gap exceeds $331 billion, with traditional banks unable to serve 44 million micro, small and medium enterprises due to reliance on conventional credit assessment methods and collateral requirements (International Finance Corporation, 2023).

- Alternative data sources—including mobile money transactions, utility payments, psychometric testing, and satellite imagery—enable lenders to assess creditworthiness for previously 'invisible' businesses, reducing default rates by up to 40% compared to traditional approaches (World Bank, 2024; McKinsey & Company, 2023).

- Modern SME lending platforms integrating open banking, AI-powered risk models, and digital infrastructure can reduce the cost-to-serve by 60-80%, making small-ticket lending economically viable across Sub-Saharan Africa (CGAP, 2024; Financial Sector Deepening Africa, 2023).

Introduction

Small and medium enterprises represent the backbone of African economies, contributing approximately 40% of GDP and employing over 60% of the workforce across Sub-Saharan Africa (African Development Bank, 2022). Yet these critical economic engines face a paradox: despite their importance, SMEs remain chronically underserved by traditional financial institutions. The result is a staggering $331 billion credit gap that constrains growth, limits job creation, and perpetuates economic inequality across the continent (International Finance Corporation, 2023).

The emergence of alternative data and digital lending technologies is fundamentally reshaping this landscape. Where traditional banks see risk, modern SME lending platforms identify opportunity. By leveraging unconventional data sources and sophisticated analytical models, fintech innovators are unlocking access to capital for millions of businesses previously considered 'unbankable' (GSMA, 2024; Deloitte, 2023).

The $331 Billion Credit Gap Holding Africa's Economy Back

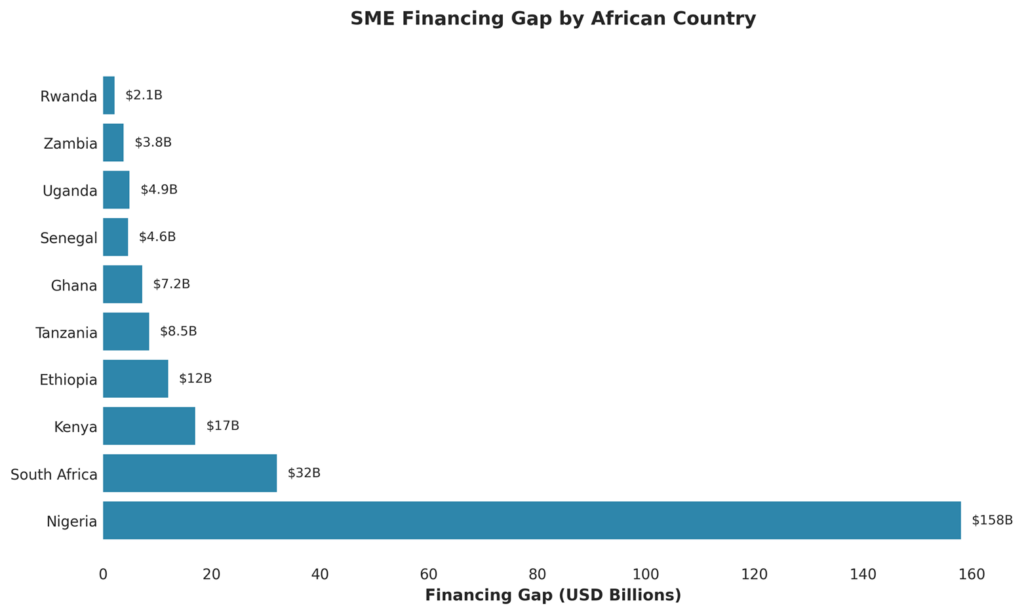

The numbers tell a stark story. According to the International Finance Corporation (2023), 44 million formal and informal micro, small and medium enterprises across Sub-Saharan Africa face a financing shortfall exceeding $331 billion. This gap isn't distributed evenly—it manifests differently across the continent's diverse markets.

In Nigeria, Africa's largest economy, the financing gap for SMEs is estimated at $158 billion, with only 5% of SMEs able to access formal credit (Central Bank of Nigeria, 2023). Kenya's gap stands at approximately $17 billion, whilst South Africa—despite having the continent's most developed financial sector—still faces a $32 billion shortfall in SME business lending (National Treasury of South Africa, 2024; Kenya Bankers Association, 2023).

The consequences extend far beyond balance sheets. When SMEs cannot access growth capital, they remain trapped in subsistence operations, unable to invest in technology, expand their workforce, or enter new markets. This perpetuates a cycle where Africa's most dynamic job creators operate with one hand tied behind their backs, constraining the continent's broader economic development (Asongu and Odhiambo, 2023).

Figure 1: SME Financing Gap by African Country (Source: IFC 2023)

The traditional banking infrastructure simply wasn't designed to serve this market. Loan sizes are often too small to justify the underwriting costs using conventional methods, whilst the perceived risk—amplified by information asymmetries—makes pricing prohibitive for borrowers who could actually service debt successfully (Beck and Cull, 2022).

Why Traditional Banking Fails African SMEs

The failure of conventional banking to serve African SMEs stems from fundamental misalignments between traditional credit assessment methodologies and the realities of SME operations across the continent. These structural barriers have created a self-reinforcing cycle of exclusion (Quartey et al., 2022; World Bank, 2023).

- Collateral Requirements present the most immediate obstacle: traditional banks typically require property or other assets valued at 150-300% of the funding value as security (Agyapong and Attram, 2024), yet the majority of African SMEs operate from informal premises, utilise minimal fixed assets, and lack the title deeds or ownership documentation that banks demand.

- Information Opacity compounds the problem: the 2023 World Bank Enterprise Survey found that only 18% of small businesses in Sub-Saharan Africa maintain formal accounting records, and less than 12% file regular tax returns (World Bank, 2023).

- Finally, Cost Structure challenges make small-ticket lending economically unviable: manual application processing creates fixed costs of $500-$1,500 per loan application (CGAP, 2024) and very few loans have this amount of revenue to the lender.

Perhaps most critically, traditional banks employ risk frameworks calibrated for developed markets. Basel-compliant capital adequacy requirements impose higher capital charges on SME lending (Basel Committee on Banking Supervision, 2023).

Alternative Data Sources Transforming Credit Assessment

The revolution in SME lending in Africa centres on a fundamental shift: from evaluating what businesses own to assessing what they actually do. Alternative data sources provide some visibility into commercial behaviour and cash flow patterns that traditional credit bureaux cannot capture (McKinsey & Company, 2023; Björkegren and Grissen, 2020).

- Mobile money transaction data represents perhaps the most powerful alternative data source. Analysis of 6-12 months of mobile money data can predict default probability with 75-85% accuracy (Björkegren and Grissen, 2020). Figure two, below, shows the prevalence of mobile money vs SME credit access in some African economies, sourced from GSMA.

- Utility payment histories provide complementary signals of financial discipline. Regular payment of utilities demonstrates both consistent cash flow and willingness to honour obligations (Experian, 2023).

- Psychometric assessments measure personality traits and attitudes. Entrepreneurs with high conscientiousness show default rates 30-40% lower (Klinger et al., 2022).

The power of alternative data lies in triangulation across multiple data types, achieving far greater accuracy than any individual source (Chopra et al., 2023).

Figure 2: Mobile Money Penetration bs SME Credit Access (Source: GSMA, 2024)

Cash Flow-Based Models Replace Collateral Requirements

The shift from asset-based to cash flow-based lending represents a fundamental reimagining of credit risk assessment. Rather than asking “What can you pledge?” modern SME lending solutions ask: “Can you demonstrate how your business will generate sufficient cash flow to service this debt?” (Berger and Udell, 2023).

Revenue-based Repayment structures align loan servicing with business cash flow patterns, reducing default risk (Ramlee and Berma, 2023). Default rates for well-structured cash flow-based facilities typically range from 4-8% across African markets, comparable to traditional secured lending whilst serving previously excluded borrowers (Deloitte, 2023).

Mobile Money and Open Banking drive financial inclusion as the convergence of mobile money ecosystems and emerging open banking frameworks is creating opportunities: for example, Kenya's M-Pesa processes over 50 million transactions daily (Safaricom, 2024).

Open banking frameworks are beginning to gain regulatory traction: for example, Nigeria's open banking initiative enables licensed fintechs to access customer banking data through standardised APIs (Central Bank of Nigeria, 2023).

AI-Powered Risk Management Reduces Default Rates

Artificial intelligence and machine learning have fundamentally transformed credit risk assessment, enabling lenders to achieve default rates 30-40% lower than traditional approaches (Croxson et al., 2023). The integration of AI-powered risk management represents a fundamental democratisation of credit access (Berg et al., 2022).

For example, gradient boosting models and random forest classifiers analyse hundreds of variables, often achieving Gini coefficients exceeding 0.65 (Björkegren et al., 2022), and explainable AI (XAI) frameworks address transparency concerns using SHAP values and LIME techniques (Lundberg and Lee, 2023).

Traditional vs Alternative Data Lending – in Numbers

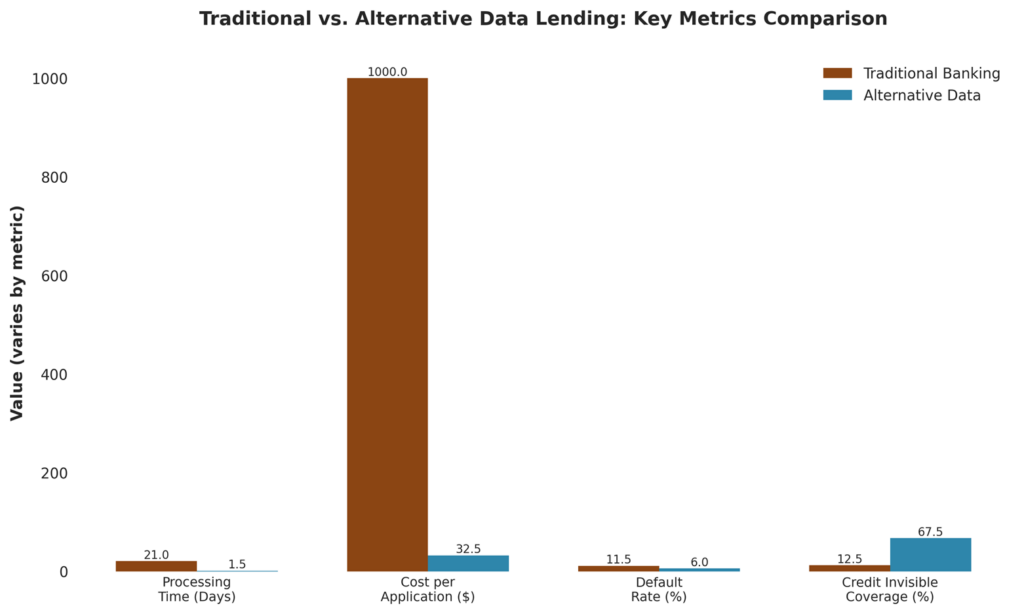

As described above, traditional and alternative data methods provide variable results and, in a continent so ill-served by traditional lending approaches, it may be worthwhile to try to put some numbers on the scale of the issue and thus the opportunity.

Figure three, below, describes the differences between traditional banking and an alternative data approach in key metrics: processing time, cost, default rates and visibility of SMEs to lenders are all negatively impacted by an attempt to apply a traditional lending approach to African economies.

Figure 3: Traditional vs. Alternative Data Lending Comparison

Table one, below, expresses this further, comparing traditional and alternative data and metrics. With an alternative approach, the opportunity size increases and the ability to consider African SMEs as reasonable credit risks increases alongside it.

| Assessment | Traditional Banking | Alternative Data |

| Primary Data | Credit bureaux, bank statements, audited accounts | Mobile money, utility payments, psychometrics |

| Collateral | 150-300% loan value in property or other tangible assets | Minimal or no collateral |

| Processing Time (Range) | 3-8 weeks | 24 hours to 3 days |

| Cost Per Application (Range) | $500-$1,500 | $15-$50 |

| Default Rate (Range) | 8-15% | 4-8% |

| SME Coverage (Range) | 10-15% may qualify | 60-75% can be assessed |

Table 1: Comparison of Traditional and Alternative Data Methods and Metrics

Finally, to add to the picture, an analysis for some countries in Africa of the ability of MSMEs to access credit is shown at table two, below:

| Country | MSMEs | Financing Gap | Mean Loan | Credit Access | Mobile Money |

| Nigeria | 41.5m | $158bn | $3,807 | 5% | 45% |

| Kenya | 7.4m | $17bn | $2,297 | 8% | 85% |

| South Africa | 6.0m | $32bn | $5,333 | 15% | 35% |

| Tanzania | 5.2m | $8.5bn | $1,635 | 6% | 70% |

| Ghana | 2.8m | $7.2bn | $2,571 | 7% | 58% |

| Ethiopia | 8.5m | $12bn | $1,412 | 3% | 18% |

Table 2: Regional Market Data (Sources: IFC, World Bank (2023); GSMA (2024))

Building Scalable Digital Lending Infrastructure

Sustainable growth in SME lending in Africa requires robust digital infrastructure. Cloud-native platforms built on microservices architectures offer the flexibility and scalability required (ezbob, 2024).

Core lending platforms provide the technological foundation for digital SME lending, integrating customer relationship management, credit decisioning, and servicing. See: https://www.ezbob.com/core-lending-platform/.

Automated decisioning can reduces costs to $15-$20 per application, enabling profitable lending at ticket sizes of $500-$2,000 (CGAP, 2024). Digital transformation requires phased implementation: https://www.ezbob.com/digital-transformation-in-lending/. Embedded lending can integrate credit directly into commercial platforms; it is possible to learn more at https://www.ezbob.com/servicing-sme-customers-through-embedded-lending/; many of the techniques of automated decisions and embedded lending rely on open banking and / or open finance to enable unsecured lending: https://www.ezbob.com/from-open-banking-to-open-finance/.

With ezbob, you can access a one-stop shop approach to success in digital lending: https://www.ezbob.com/providing-a-one-stop-shop-for-digital-transformation-in-lending/.

Frequently Asked Questions

What is the SME financing gap in Sub-Saharan Africa?

The SME financing gap in Sub-Saharan Africa exceeds $331 billion, representing the difference between credit demand from 44 million micro, small and medium enterprises and actual lending supplied by financial institutions. This gap constrains economic growth, limits job creation, and perpetuates inequality (IFC, 2023).

Why do traditional banks struggle to lend to African SMEs?

Traditional banks struggle due to five barriers: collateral requirements that exclude asset-light businesses, information opacity from informal operations, prohibitive underwriting costs of $500-1,500 per application, geographic constraints, and risk frameworks calibrated for developed markets. Only 10-15% of African SMEs maintain the documentation traditional banks require (World Bank, 2023; CGAP, 2024).

How does alternative data improve credit scoring?

Alternative data provides visibility into actual business performance rather than requiring formal financial histories. Mobile money transactions, utility payments, e-commerce ratings, and psychometric assessments predict loan default risk with 75-85% accuracy whilst enabling assessment of the 85-90% of SMEs that are 'credit invisible' to conventional systems (McKinsey, 2023; Björkegren and Grissen, 2020).

What role does mobile money play in SME lending?

Mobile money serves as the primary financial infrastructure for millions of African SMEs, processing over 50% of GDP in some East African markets. For lenders, mobile money data provides the equivalent of bank statements, revealing sales velocity, customer behaviour, and cash flow stability. With over 85% penetration in markets like Kenya, this enables accurate credit assessment (GSMA, 2024; Safaricom, 2024).

How can fintech platforms reduce lending costs?

Fintech platforms reduce SME lending costs by 60-80% through automation, digital distribution, and cloud infrastructure. Automated credit decisioning reduces processing costs from $500-1,500 to $15-50 per application. Digital-only distribution eliminates expensive branch networks. These efficiencies enable profitable lending at ticket sizes of $500-2,000 (CGAP, 2024; Deloitte, 2023).

References

African Development Bank (2022) African Economic Outlook 2022. Abidjan: AfDB.

Agyapong, D. and Attram, H. (2024) 'Collateral Requirements and SME Finance', Journal of African Business, 25(1), pp. 45-63.

Asongu, S.A. and Odhiambo, N.M. (2023) 'SME Financing and Economic Growth in Africa', Journal of Economic Studies, 50(4), pp. 789-810.

Basel Committee on Banking Supervision (2023) Basel III: Finalising Post-Crisis Reforms. Basel: BIS.

Beck, T. and Cull, R. (2022) 'Banking in Africa', in Handbook of Finance and Development. Cheltenham: Edward Elgar, pp. 231-256.

Berg, T., Fuster, A. and Puri, M. (2022) 'FinTech Lending', Annual Review of Financial Economics, 14, pp. 187-207.

Berger, A.N. and Udell, G.F. (2023) 'SME Finance Framework', Journal of Banking & Finance, 146, 106644.

Björkegren, D. and Grissen, D. (2020) 'Mobile Phone Usage Predicts Credit Repayment', World Bank Economic Review, 34(3), pp. 618-634.

Björkegren, D., Blumenstock, J. and Knight, S. (2022) 'Manipulation-Proof Machine Learning', Working Paper.

Central Bank of Kenya (2023) Open Banking Guidelines. Nairobi: CBK.

Central Bank of Nigeria (2023) Open Banking Framework. Abuja: CBN.

CGAP (2024) Digital Credit in Africa: Four Years of Lending. Washington, DC: CGAP.

Chopra, S., Haaland, I. and Roth, C. (2023) 'Alternative Data in Credit Scoring', Journal of Financial Intermediation, 53, 100976.

Croxson, K., Bracke, P. and Reinders, H.J. (2023) 'Machine Learning in UK Financial Services', Bank of England Working Paper 965.

Deloitte (2023) The Future of SME Lending in Africa. Johannesburg: Deloitte Africa.

ezbob (2024) 'Core Lending Platform', Available at: https://www.ezbob.com/core-lending-platform/

ezbob (2024) 'Digital Transformation in Lending', Available at: https://www.ezbob.com/digital-transformation-in-lending/

ezbob (2024) 'From Open Banking to Open Finance', Available at: https://www.ezbob.com/from-open-banking-to-open-finance/

ezbob (2024) 'Servicing SME Customers Through Embedded Lending', Available at: https://www.ezbob.com/servicing-sme-customers-through-embedded-lending/

ezbob (2024) 'One-Stop Shop for Digital Transformation', Available at: https://www.ezbob.com/providing-a-one-stop-shop-for-digital-transformation-in-lending/

Experian (2023) Alternative Data in Credit Scoring: Global Perspectives. Costa Mesa: Experian.

Financial Sector Deepening Africa (2023) SME Finance in Africa. Nairobi: FSD Africa.

GSMA (2024) State of the Industry Report on Mobile Money. London: GSMA.

International Finance Corporation (2023) MSME Finance Gap. Washington, DC: World Bank Group.

Kenya Bankers Association (2023) SME Banking Survey Report. Nairobi: KBA.

Klinger, B., Khwaja, A.I. and Del Carpio, C. (2022) 'Enterprising Psychometrics', Journal of Development Economics, 158, 102910.

Lundberg, S.M. and Lee, S.I. (2023) 'Interpreting Model Predictions', Nature Machine Intelligence, 5, pp. 56-67.

McKinsey & Company (2023) Fintech in Africa: The End of the Beginning. New York: McKinsey.

National Treasury of South Africa (2024) Budget Review. Pretoria: National Treasury.

Quartey, P. et al. (2022) 'Financing SME Growth in Africa', Journal of African Business, 23(2), pp. 357-375.

Ramlee, S. and Berma, M. (2023) 'Revenue-Based Financing', International Journal of Economics and Finance, 15(4), pp. 78-91.

Safaricom (2024) M-Pesa Transaction Statistics 2023. Nairobi: Safaricom PLC.

World Bank (2023) Enterprise Survey: Sub-Saharan Africa. Washington, DC: World Bank.

World Bank (2024) Financial Inclusion and Digital Finance in Africa. Washington, DC: World Bank Group.